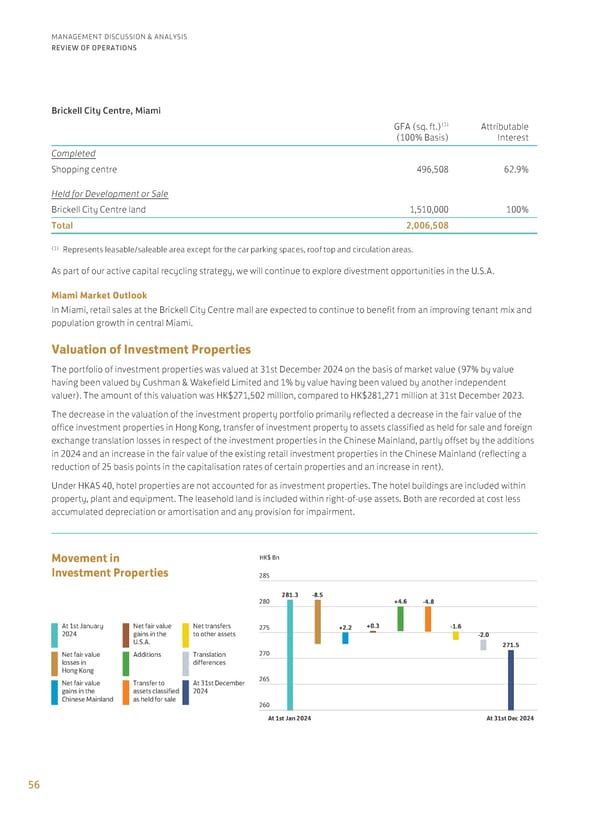

285 265 270 260 275 280 281.3 -8.5 +2.2 +0.3 -4.8 +4.6 -2.0 271.5 -1.6 HK$ Bn At 1st Jan 2024 At 31st Dec 2024 Movement in Investment Properties At 1st January 2024 Net fair value losses in Hong Kong Net fair value gains in the Chinese Mainland Net fair value gains in the U.S.A. Additions Transfer to assets classified as held for sale Net transfers to other assets Translation differences At 31st December 2024 56 MANAGEMENT DISCUSSION & ANALYSIS REVIEW OF OPERATIONS Brickell City Centre, Miami GFA (sq. ft.)(1) (100% Basis) Attributable Interest Completed Shopping centre 496,508 62.9% Held for Development or Sale Brickell City Centre land 1,510,000 100% Total 2,006,508 (1) Represents leasable/saleable area except for the car parking spaces, roof top and circulation areas. As part of our active capital recycling strategy, we will continue to explore divestment opportunities in the U.S.A. Miami Market Outlook In Miami, retail sales at the Brickell City Centre mall are expected to continue to benefit from an improving tenant mix and population growth in central Miami. Valuation of Investment Properties The portfolio of investment properties was valued at 31st December 2024 on the basis of market value (97% by value having been valued by Cushman & Wakefield Limited and 1% by value having been valued by another independent valuer). The amount of this valuation was HK$271,502 million, compared to HK$281,271 million at 31st December 2023. The decrease in the valuation of the investment property portfolio primarily reflected a decrease in the fair value of the office investment properties in Hong Kong, transfer of investment property to assets classified as held for sale and foreign exchange translation losses in respect of the investment properties in the Chinese Mainland, partly offset by the additions in 2024 and an increase in the fair value of the existing retail investment properties in the Chinese Mainland (reflecting a reduction of 25 basis points in the capitalisation rates of certain properties and an increase in rent). Under HKAS 40, hotel properties are not accounted for as investment properties. The hotel buildings are included within property, plant and equipment. The leasehold land is included within right-of-use assets. Both are recorded at cost less accumulated depreciation or amortisation and any provision for impairment.

Annual Report 2024 | EN Page 57 Page 59

Annual Report 2024 | EN Page 57 Page 59