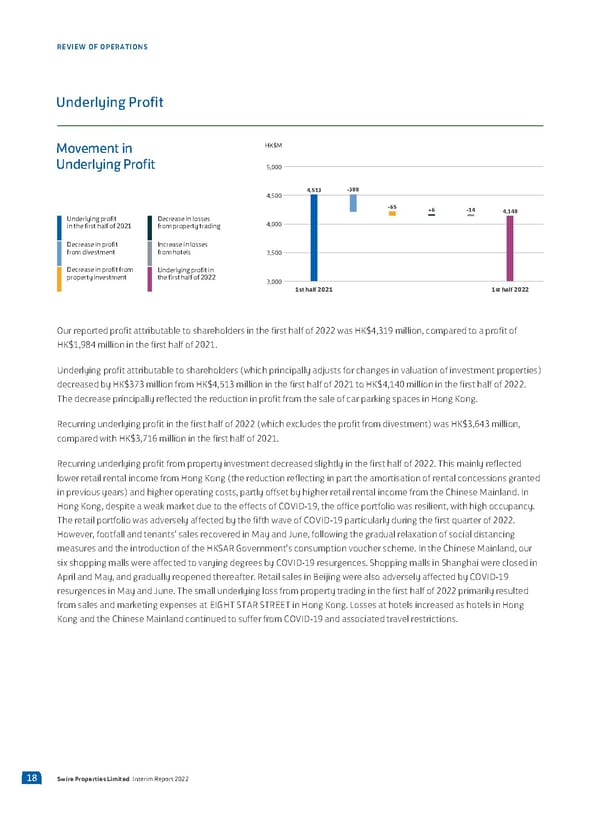

REVIEW OF OPERATIONS Underlying Profit Movement in M Underlying Profit 5,000 4,500 4,513 -300 -65 +6 -14 4,140 Underlying profit Decrease in losses 4,000 in the first half of 2021 from property trading Decrease in profit Increase in losses from divestment from hotels 3,500 Decrease in profit from Underlying profit in property investment the first half of 2022 3,000 1st half 2021 1st half 2022 Our reported profit attributable to shareholders in the first half of 2022 was HK$4,319 million, compared to a profit of HK$1,984 million in the first half of 2021. Underlying profit attributable to shareholders (which principally adjusts for changes in valuation of investment properties) decreased by HK$373 million from HK$4,513 million in the first half of 2021 to HK$4,140 million in the first half of 2022. The decrease principally reflected the reduction in profit from the sale of car parking spaces in Hong Kong. Recurring underlying profit in the first half of 2022 (which excludes the profit from divestment) was HK$3,643 million, compared with HK$3,716 million in the first half of 2021. Recurring underlying profit from property investment decreased slightly in the first half of 2022. This mainly reflected lower retail rental income from Hong Kong (the reduction reflecting in part the amortisation of rental concessions granted in previous years) and higher operating costs, partly offset by higher retail rental income from the Chinese Mainland. In Hong Kong, despite a weak market due to the effects of COVID-19, the office portfolio was resilient, with high occupancy. The retail portfolio was adversely affected by the fifth wave of COVID-19 particularly during the first quarter of 2022. However, footfall and tenants’ sales recovered in May and June, following the gradual relaxation of social distancing measures and the introduction of the HKSAR Government’s consumption voucher scheme. In the Chinese Mainland, our six shopping malls were affected to varying degrees by COVID-19 resurgences. Shopping malls in Shanghai were closed in April and May, and gradually reopened thereafter. Retail sales in Beijing were also adversely affected by COVID-19 resurgences in May and June. The small underlying loss from property trading in the first half of 2022 primarily resulted from sales and marketing expenses at EIGHT STAR STREET in Hong Kong. Losses at hotels increased as hotels in Hong Kong and the Chinese Mainland continued to suffer from COVID-19 and associated travel restrictions. 18 Swire Properties Limited Interim Report 2022

2022 Interim Report Page 19 Page 21

2022 Interim Report Page 19 Page 21