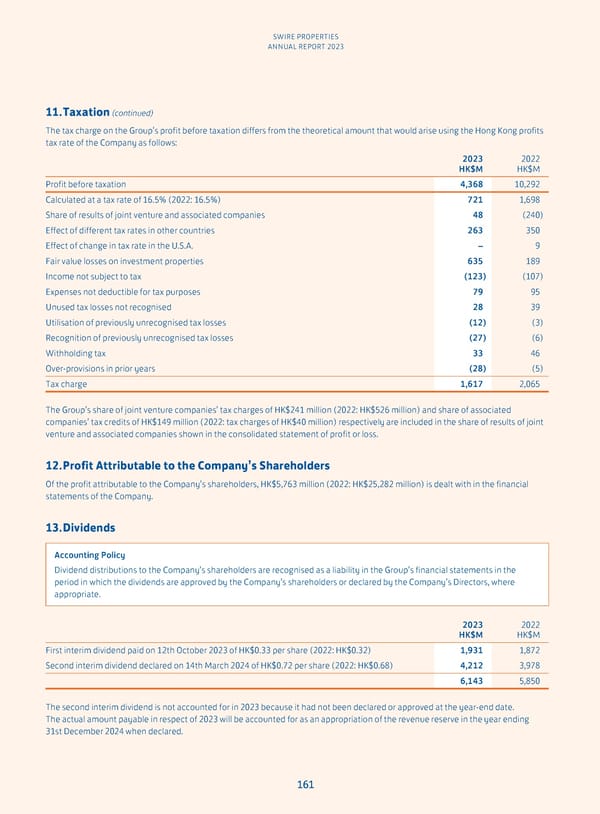

SWIRE PROPERTIES ANNUAL REPORT 2023 11. Taxation (continued) The tax charge on the Group’s profit before taxation differs from the theoretical amount that would arise using the Hong Kong profits tax rate of the Company as follows: 2023 2022 HK$M HK$M Profit before taxation 4,368 10,292 Calculated at a tax rate of 16.5% (2022: 16.5%) 721 1,698 Share of results of joint venture and associated companies 48 (240) Effect of different tax rates in other countries 263 350 Effect of change in tax rate in the U.S.A. – 9 Fair value losses on investment properties 635 189 Income not subject to tax (123) (107) Expenses not deductible for tax purposes 79 95 Unused tax losses not recognised 28 39 Utilisation of previously unrecognised tax losses (12) (3) Recognition of previously unrecognised tax losses (27) (6) Withholding tax 33 46 Over-provisions in prior years (28) (5) Tax charge 1,617 2,065 The Group’s share of joint venture companies’ tax charges of HK$241 million (2022: HK$526 million) and share of associated companies’ tax credits of HK$149 million (2022: tax charges of HK$40 million) respectively are included in the share of results of joint venture and associated companies shown in the consolidated statement of profit or loss. 12. Profit Attributable to the Company’s Shareholders Of the profit attributable to the Company’s shareholders, HK$5,763 million (2022: HK$25,282 million) is dealt with in the financial statements of the Company. 13. Dividends Accounting Policy Dividend distributions to the Company’s shareholders are recognised as a liability in the Group’s financial statements in the period in which the dividends are approved by the Company’s shareholders or declared by the Company’s Directors, where appropriate. 2023 2022 HK$M HK$M First interim dividend paid on 12th October 2023 of HK$0.33 per share (2022: HK$0.32) 1,931 1,872 Second interim dividend declared on 14th March 2024 of HK$0.72 per share (2022: HK$0.68) 4,212 3,978 6,143 5,850 The second interim dividend is not accounted for in 2023 because it had not been declared or approved at the year-end date. The actual amount payable in respect of 2023 will be accounted for as an appropriation of the revenue reserve in the year ending 31st December 2024 when declared. 161

Annual Report 2023 Page 162 Page 164

Annual Report 2023 Page 162 Page 164