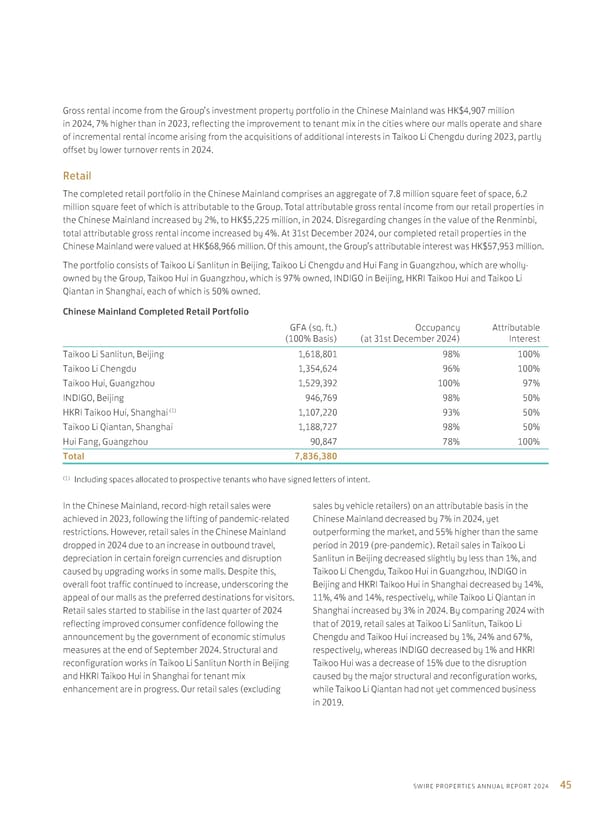

45 SWIRE PROPERTIES ANNUAL REPORT 2024 Gross rental income from the Group’s investment property portfolio in the Chinese Mainland was HK$4,907 million in 2024, 7% higher than in 2023, reflecting the improvement to tenant mix in the cities where our malls operate and share of incremental rental income arising from the acquisitions of additional interests in Taikoo Li Chengdu during 2023, partly offset by lower turnover rents in 2024. Retail The completed retail portfolio in the Chinese Mainland comprises an aggregate of 7.8 million square feet of space, 6.2 million square feet of which is attributable to the Group. Total attributable gross rental income from our retail properties in the Chinese Mainland increased by 2%, to HK$5,225 million, in 2024. Disregarding changes in the value of the Renminbi, total attributable gross rental income increased by 4%. At 31st December 2024, our completed retail properties in the Chinese Mainland were valued at HK$68,966 million. Of this amount, the Group’s attributable interest was HK$57,953 million. The portfolio consists of Taikoo Li Sanlitun in Beijing, Taikoo Li Chengdu and Hui Fang in Guangzhou, which are wholly- owned by the Group, Taikoo Hui in Guangzhou, which is 97% owned, INDIGO in Beijing, HKRI Taikoo Hui and Taikoo Li Qiantan in Shanghai, each of which is 50% owned. Chinese Mainland Completed Retail Portfolio GFA (sq. ft.) (100% Basis) Occupancy (at 31st December 2024) Attributable Interest Taikoo Li Sanlitun, Beijing 1,618,801 98% 100% Taikoo Li Chengdu 1,354,624 96% 100% Taikoo Hui, Guangzhou 1,529,392 100% 97% INDIGO, Beijing 946,769 98% 50% HKRI Taikoo Hui, Shanghai (1) 1,107,220 93% 50% Taikoo Li Qiantan, Shanghai 1,188,727 98% 50% Hui Fang, Guangzhou 90,847 78% 100% Total 7,836,380 (1) Including spaces allocated to prospective tenants who have signed letters of intent. In the Chinese Mainland, record-high retail sales were achieved in 2023, following the lifting of pandemic-related restrictions. However, retail sales in the Chinese Mainland dropped in 2024 due to an increase in outbound travel, depreciation in certain foreign currencies and disruption caused by upgrading works in some malls. Despite this, overall foot traffic continued to increase, underscoring the appeal of our malls as the preferred destinations for visitors. Retail sales started to stabilise in the last quarter of 2024 reflecting improved consumer confidence following the announcement by the government of economic stimulus measures at the end of September 2024. Structural and reconfiguration works in Taikoo Li Sanlitun North in Beijing and HKRI Taikoo Hui in Shanghai for tenant mix enhancement are in progress. Our retail sales (excluding sales by vehicle retailers) on an attributable basis in the Chinese Mainland decreased by 7% in 2024, yet outperforming the market, and 55% higher than the same period in 2019 (pre-pandemic). Retail sales in Taikoo Li Sanlitun in Beijing decreased slightly by less than 1%, and Taikoo Li Chengdu, Taikoo Hui in Guangzhou, INDIGO in Beijing and HKRI Taikoo Hui in Shanghai decreased by 14%, 11%, 4% and 14%, respectively, while Taikoo Li Qiantan in Shanghai increased by 3% in 2024. By comparing 2024 with that of 2019, retail sales at Taikoo Li Sanlitun, Taikoo Li Chengdu and Taikoo Hui increased by 1%, 24% and 67%, respectively, whereas INDIGO decreased by 1% and HKRI Taikoo Hui was a decrease of 15% due to the disruption caused by the major structural and reconfiguration works, while Taikoo Li Qiantan had not yet commenced business in 2019.

Annual Report 2024 | EN Page 46 Page 48

Annual Report 2024 | EN Page 46 Page 48