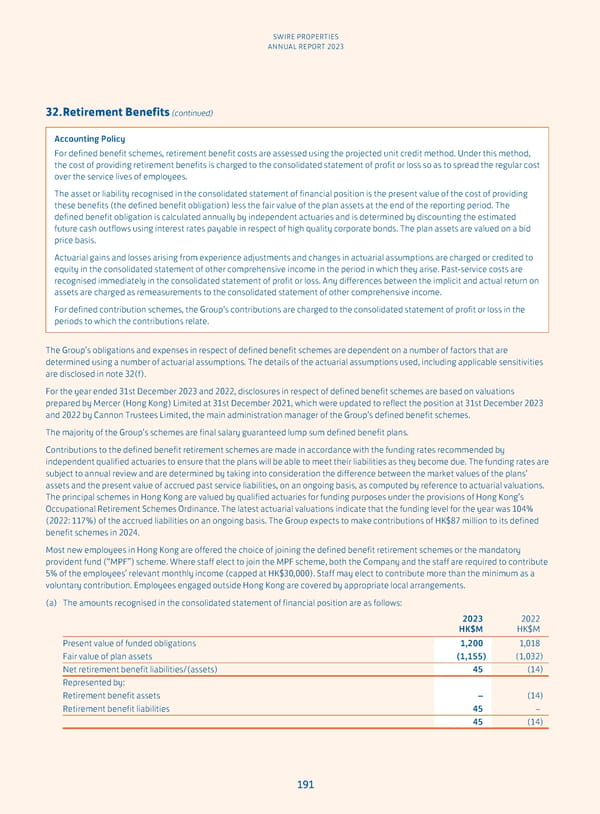

SWIRE PROPERTIES ANNUAL REPORT 2023 32. Retirement Benefits (continued) Accounting Policy For defined benefit schemes, retirement benefit costs are assessed using the projected unit credit method. Under this method, the cost of providing retirement benefits is charged to the consolidated statement of profit or loss so as to spread the regular cost over the service lives of employees. The asset or liability recognised in the consolidated statement of financial position is the present value of the cost of providing these benefits (the defined benefit obligation) less the fair value of the plan assets at the end of the reporting period. The defined benefit obligation is calculated annually by independent actuaries and is determined by discounting the estimated future cash outflows using interest rates payable in respect of high quality corporate bonds. The plan assets are valued on a bid price basis. Actuarial gains and losses arising from experience adjustments and changes in actuarial assumptions are charged or credited to equity in the consolidated statement of other comprehensive income in the period in which they arise. Past-service costs are recognised immediately in the consolidated statement of profit or loss. Any differences between the implicit and actual return on assets are charged as remeasurements to the consolidated statement of other comprehensive income. For defined contribution schemes, the Group’s contributions are charged to the consolidated statement of profit or loss in the periods to which the contributions relate. The Group’s obligations and expenses in respect of defined benefit schemes are dependent on a number of factors that are determined using a number of actuarial assumptions. The details of the actuarial assumptions used, including applicable sensitivities are disclosed in note 32(f). For the year ended 31st December 2023 and 2022, disclosures in respect of defined benefit schemes are based on valuations prepared by Mercer (Hong Kong) Limited at 31st December 2021, which were updated to reflect the position at 31st December 2023 and 2022 by Cannon Trustees Limited, the main administration manager of the Group’s defined benefit schemes. The majority of the Group’s schemes are final salary guaranteed lump sum defined benefit plans. Contributions to the defined benefit retirement schemes are made in accordance with the funding rates recommended by independent qualified actuaries to ensure that the plans will be able to meet their liabilities as they become due. The funding rates are subject to annual review and are determined by taking into consideration the difference between the market values of the plans’ assets and the present value of accrued past service liabilities, on an ongoing basis, as computed by reference to actuarial valuations. The principal schemes in Hong Kong are valued by qualified actuaries for funding purposes under the provisions of Hong Kong’s Occupational Retirement Schemes Ordinance. The latest actuarial valuations indicate that the funding level for the year was 104% (2022: 117%) of the accrued liabilities on an ongoing basis. The Group expects to make contributions of HK$87 million to its defined benefit schemes in 2024. Most new employees in Hong Kong are offered the choice of joining the defined benefit retirement schemes or the mandatory provident fund (“MPF”) scheme. Where staff elect to join the MPF scheme, both the Company and the staff are required to contribute 5% of the employees’ relevant monthly income (capped at HK$30,000). Staff may elect to contribute more than the minimum as a voluntary contribution. Employees engaged outside Hong Kong are covered by appropriate local arrangements. The amounts recognised in the consolidated statement of financial position are as follows: (a) 2023 2022 HK$M HK$M Present value of funded obligations 1,200 1,018 Fair value of plan assets (1,155) (1,032) Net retirement benefit liabilities/(assets) 45 (14) Represented by: Retirement benefit assets – (14) Retirement benefit liabilities 45 – 45 (14) 191

Annual Report 2023 Page 192 Page 194

Annual Report 2023 Page 192 Page 194