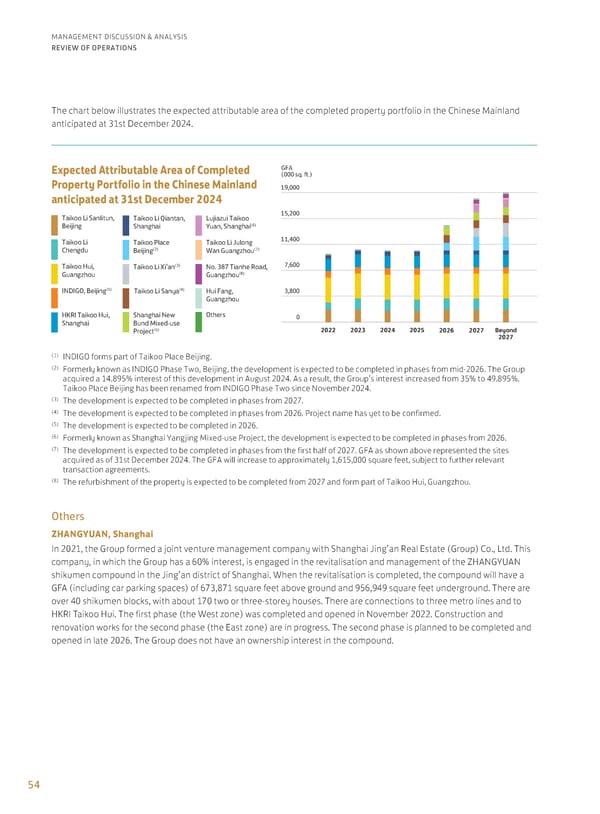

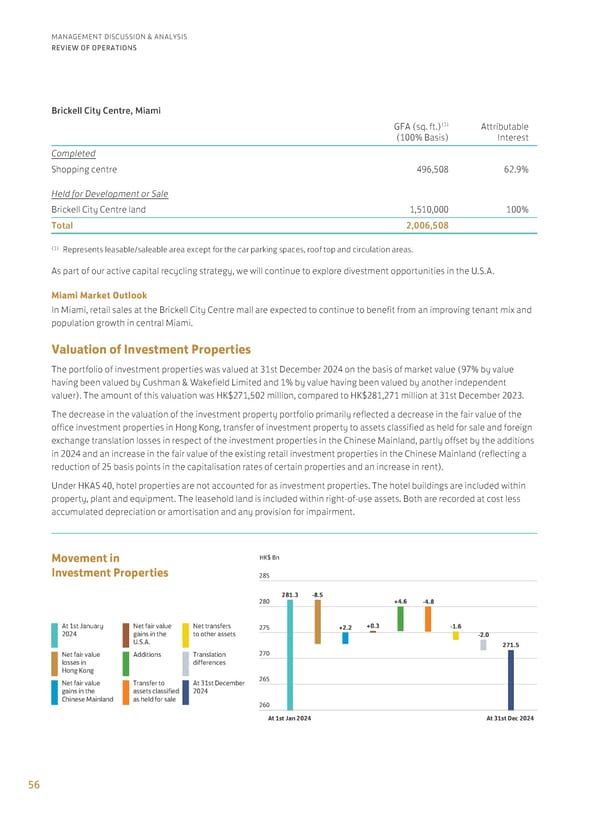

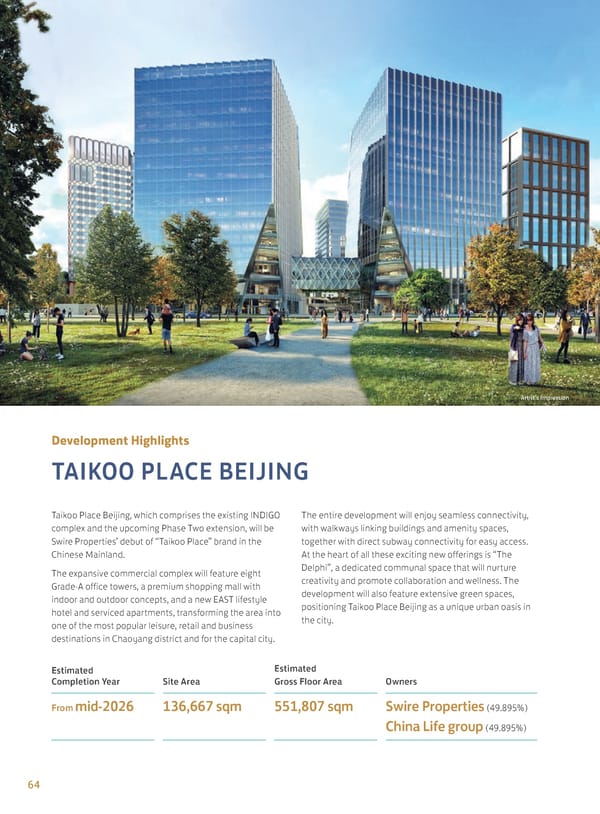

Annual Report 2024 | EN

ANNUAL REPORT 2024 Stock Code: 01972

3 Company Profile 6 2024 Highlights 12 Financial Highlights 13 Ten-Year Financial Summary 16 Chairman’s Statement 19 Chief Executive’s Statement 24 Key Business Strategies 28 Review of Operations 74 Financial Review 81 Financing 92 Corporate Governance 110 Risk Management 117 Directors and Officers 119 Directors’ Report 125 Sustainability Review CONTENTS 134 Independent Auditor’s Report 138 Consolidated Statement of Profit or Loss 139 Consolidated Statement of Other Comprehensive Income 140 Consolidated Statement of Financial Position 141 Consolidated Statement of Cash Flows 142 Consolidated Statement of Changes in Equity 143 Notes to the Financial Statements 199 Accounting Policies 202 Principal Subsidiary, Joint Venture and Associated Companies 205 Schedule of Principal Group Properties 215 Glossary 216 Financial Calendar and Information for Investors MANAGEMENT DISCUSSION & ANALYSIS CORPORATE GOVERNANCE & SUSTAINABILITY AUDITOR’S REPORT AND ACCOUNTS SUPPLEMENTARY INFORMATION

3 SWIRE PROPERTIES ANNUAL REPORT 2024 COMPANY PROFILE Swire Properties Limited (the “Company”) is a leading developer, owner and operator of mixed-use, principally commercial, properties in Hong Kong and the Chinese Mainland, with a record of creating long-term value by placemaking and transforming urban areas. Our business comprises three elements: property investment, property trading, and hotel investment and management. Founded in Hong Kong in 1972, the Company is listed on The Stock Exchange of Hong Kong Limited and, with its subsidiaries, employs around 5,800 people. The Company’s shopping malls are home to more than 2,200 retail outlets. Its offices house a working population estimated to exceed 70,000. In Hong Kong, we have spent over 50 years developing an industrial area into what is now Taikoo Place and Cityplaza, one of Hong Kong’s largest business districts comprising office space, the largest shopping mall on Hong Kong Island and a hotel. Pacific Place, built on the former Victoria Barracks site, is one of Hong Kong’s premier retail and business addresses. In the Chinese Mainland, the Company has six major commercial projects in operation in Beijing, Guangzhou, Chengdu and Shanghai, and has several projects under development in Beijing, Guangzhou, Shanghai, Sanya and Xi’an. Similar in scale to our developments in Hong Kong, our Chinese Mainland properties are in prime locations with excellent transport connections. The Company has interests in the luxury and high-quality residential markets in Hong Kong, the Chinese Mainland, Indonesia, Vietnam and Thailand. There are also land banks in Miami, U.S.A. Swire Hotels develops and manages hotels in Hong Kong, the Chinese Mainland and the U.S.A., with a confirmed expansion plan to Japan. The Company has a presence in the Brickell financial district in Miami, U.S.A., where it has investment properties. The Company has offices in South East Asia which explore opportunities in the property markets in the region.

CREATIVE TRANSFORMATION Captures what we do and how we do it. It underlines the creative mindset and long-term approach that enables us to seek out new perspectives, and original thinking that goes beyond the conventional. It also encapsulates our ability to unlock the potential of places and create vibrant destinations that can engender further growth and create sustainable value for our stakeholders.

6 2024 HIGHLIGHTS 04 Partnered with the Taskforce on Nature- related Financial Disclosures to launch its nature-related risk management and disclosure framework in Hong Kong. Hong Kong 03 In Swire Properties’ Arts Month, SHELF II was debuted at Taikoo Place as a permanent installation; Enchanted Forest and Valkyrie Seondeok were hosted at ArtisTree and Two Taikoo Place respectively. Entering the twelfth year of partnership with Art Basel Hong Kong, Pacific Place showcased Doan, an offsite art installation from the fair’s Encounters sector. Hong Kong 06 Deloitte China renewed a 10-year lease as anchor tenant of One Pacific Place. Hong Kong Acquired 50% stake in Taikoo Li Julong Wan Guangzhou, a retail portion of the mixed-use development. Guangzhou 08 Announced a share buy-back programme of up to HK$1.5 billion until May 2025. Hong Kong Successfully bid for No.387 Tianhe Road which will be renovated as a luxury retail addition to Taikoo Hui Guangzhou. Guangzhou 11 Revealed the plans to rename the existing, mixed-use INDIGO development with its Phase Two extension as Taikoo Place Beijing, marking the debut of the “Taikoo Place” brand in the Chinese Mainland. Beijing Artist’s Impression

7 SWIRE PROPERTIES ANNUAL REPORT 2024 11 Announced the completion of the 10-year Taikoo Place Redevelopment Project, which introduced two triple Grade-A office towers, Taikoo Square and Taikoo Garden, and new air-conditioned elevated walkways. Hong Kong 11 LVMH and Swire Properties formed a partnership to improve their ESG performance across LVMH stores, offices and F&B locations in the Chinese Mainland and Hong Kong. Hong Kong and Chinese Mainland 12 Launched the pre-sales at Lujiazui Taikoo Yuan Residences in Shanghai, the Company’s first residential project in the Chinese Mainland, which received an overwhelming response. Shanghai 01 2025 Rose to the top position globally in the Dow Jones Best-in-Class World Index 2024 in the Real Estate Management & Development Industry category, realising the Company’s SD 2030 vision six years ahead of schedule. 03 2025 Announced the name Taikoo Li Julong Wan Guangzhou, a new cultural and commercial landmark in the Greater Bay Area. Guangzhou Artist’s Impression Artist’s Impression

“Our vision is to be the leading sustainable development performer in our industry globally by 2030.” – GUY BRADLEY, CHAIRMAN 2024 SUSTAINABLE DEVELOPMENT HIGHLIGHTS 2024 HIGHLIGHTS

9 SWIRE PROPERTIES ANNUAL REPORT 2024 Ranked 1st globally in the Real Estate Management and Development Industry category Dow Jones Best-in-Class World Index constituent company for the 8th consecutive year Global Sector Leader – Listed (Mixed Use) for the 8th consecutive year Global Development Sector Leader (Mixed Use) for the 5th consecutive year No. 1 for the 7th consecutive year and maintained the highest “AAA” rating S&P Sustainability Yearbook 2025 Top 1% S&P Global ESG Score in the Real Estate Management and Development industry S&P Sustainability Yearbook (China) 2024 Top 1% S&P Global ESG Score (China) in the Real Estate Management and Development industry SEHK:1972 2024-2025 Hong Kong Management Association 2024 Best Annual Reports Awards Sustainability Report 2023: Best Environmental, Social and Governance Reporting Award (Property Development & Investment industry); Annual Report 2023: Gold Award (General category) Hong Kong Institute of Certified Public Accountants Best Corporate Governance and ESG Awards 2024 Sustainability Report 2023: ESG Award (Top Accolade) in the Non-Hang Seng Index (Large Market Capitalisation) Category Randstad Hong Kong Employer Brand Awards 2024 Most Attractive Employer in the Property and Real Estate Sector Human Resources Online HR Distinction Awards 2024 “Gold” – Excellence in Strategic Talent Attraction RICS Hong Kong Awards 2024 Taikoo Place: Environmental Impact Award LEED v4.1 for Communities: Existing Communities Taikoo Place: The first and only project in the Greater Bay Area to achieve Platinum certification (as at Dec 2024) LEED “Campaign: Frontiers” Programme Two Taikoo Place: The first and only Hong Kong project to be included in the 2024 Sustainable Frontiers List (as at Dec 2024) LEED Zero Certification Taikoo Hui, Guangzhou (Tower 2): The second and largest mixed-use office project globally (in terms of office building gross floor area) and the first mixed-use Chinese Mainland office to achieve LEED Zero Carbon and LEED Zero Energy certifications INDIGO: The first development in the Chinese Mainland to receive LEED Zero Water certification sector leader 2024

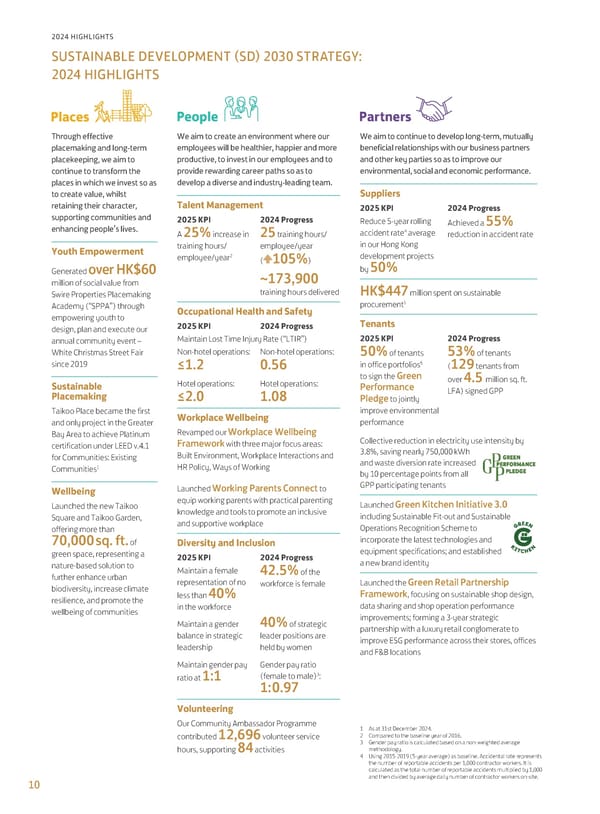

10 SUSTAINABLE DEVELOPMENT (SD) 2030 STRATEGY: 2024 HIGHLIGHTS 2024 HIGHLIGHTS Through effective placemaking and long-term placekeeping, we aim to continue to transform the places in which we invest so as to create value, whilst retaining their character, supporting communities and enhancing people’s lives. Youth Empowerment Generated over HK$60 million of social value from Swire Properties Placemaking Academy (“SPPA”) through empowering youth to design, plan and execute our annual community event – White Christmas Street Fair since 2019 Sustainable Placemaking Taikoo Place became the first and only project in the Greater Bay Area to achieve Platinum certification under LEED v.4.1 for Communities: Existing Communities1 Wellbeing Launched the new Taikoo Square and Taikoo Garden, offering more than 70,000 sq. ft. of green space, representing a nature-based solution to further enhance urban biodiversity, increase climate resilience, and promote the wellbeing of communities We aim to create an environment where our employees will be healthier, happier and more productive, to invest in our employees and to provide rewarding career paths so as to develop a diverse and industry-leading team. Talent Management 2025 KPI A 25% increase in training hours/ employee/year2 2024 Progress 25 training hours/ employee/year ( 105%) ~173,900 training hours delivered Occupational Health and Safety 2025 KPI 2024 Progress Maintain Lost Time Injury Rate (“LTIR”) Non-hotel operations: ≤1.2 Hotel operations: ≤2.0 Non-hotel operations: 0.56 Hotel operations: 1.08 Workplace Wellbeing Revamped our Workplace Wellbeing Framework with three major focus areas: Built Environment, Workplace Interactions and HR Policy, Ways of Working Launched Working Parents Connect to equip working parents with practical parenting knowledge and tools to promote an inclusive and supportive workplace Diversity and Inclusion 2025 KPI Maintain a female representation of no less than 40% in the workforce Maintain a gender balance in strategic leadership Maintain gender pay ratio at 1:1 2024 Progress 42.5% of the workforce is female 40% of strategic leader positions are held by women Gender pay ratio (female to male)3: 1:0.97 Volunteering Our Community Ambassador Programme contributed 12,696 volunteer service hours, supporting 84 activities We aim to continue to develop long-term, mutually beneficial relationships with our business partners and other key parties so as to improve our environmental, social and economic performance. Suppliers 2025 KPI Reduce 5-year rolling accident rate4 average in our Hong Kong development projects by 50% 2024 Progress Achieved a 55% reduction in accident rate HK$447 million spent on sustainable procurement5 Tenants 2025 KPI 50% of tenants in office portfolios6 to sign the Green Performance Pledge to jointly improve environmental performance 2024 Progress 53% of tenants (129 tenants from over 4.5 million sq. ft. LFA) signed GPP Collective reduction in electricity use intensity by 3.8%, saving nearly 750,000 kWh and waste diversion rate increased by 10 percentage points from all GPP participating tenants Launched Green Kitchen Initiative 3.0 including Sustainable Fit-out and Sustainable Operations Recognition Scheme to incorporate the latest technologies and equipment specifications; and established a new brand identity Launched the Green Retail Partnership Framework, focusing on sustainable shop design, data sharing and shop operation performance improvements; forming a 3-year strategic partnership with a luxury retail conglomerate to improve ESG performance across their stores, offices and F&B locations 1 As at 31st December 2024. 2 Compared to the baseline year of 2016. 3 Gender pay ratio is calculated based on a non-weighted average methodology. 4 Using 2015-2019 (5-year average) as baseline. Accidental rate represents the number of reportable accidents per 1,000 contractor workers. It is calculated as the total number of reportable accidents multiplied by 1,000 and then divided by average daily number of contractor workers on-site. Places People Partners Performance (Environment) Performance (Economic) Places People Partners Performance (Environment) Performance (Economic)

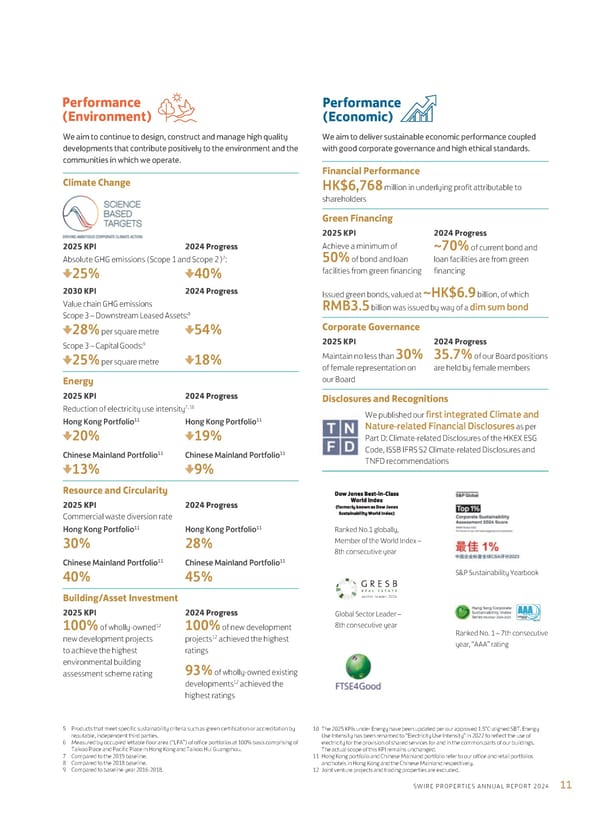

11 SWIRE PROPERTIES ANNUAL REPORT 2024 We aim to continue to design, construct and manage high quality developments that contribute positively to the environment and the communities in which we operate. Climate Change 2025 KPI 2024 Progress Absolute GHG emissions (Scope 1 and Scope 2)7: 25% 40% 2030 KPI 2024 Progress Value chain GHG emissions Scope 3 – Downstream Leased Assets:8 28% per square metre 54% Scope 3 – Capital Goods:9 25% per square metre 18% Energy 2025 KPI 2024 Progress Reduction of electricity use intensity7, 10 Hong Kong Portfolio11 20% Chinese Mainland Portfolio11 13% Hong Kong Portfolio11 19% Chinese Mainland Portfolio11 9% Resource and Circularity 2025 KPI 2024 Progress Commercial waste diversion rate Hong Kong Portfolio11 30% Chinese Mainland Portfolio11 40% Hong Kong Portfolio11 28% Chinese Mainland Portfolio11 45% Building/Asset Investment 2025 KPI 100% of wholly-owned12 new development projects to achieve the highest environmental building assessment scheme rating 2024 Progress 100% of new development projects12 achieved the highest ratings 93% of wholly-owned existing developments12 achieved the highest ratings We aim to deliver sustainable economic performance coupled with good corporate governance and high ethical standards. Financial Performance HK$6,768 million in underlying profit attributable to shareholders Green Financing 2025 KPI Achieve a minimum of 50% of bond and loan facilities from green financing 2024 Progress ~70% of current bond and loan facilities are from green financing Issued green bonds, valued at ~HK$6.9 billion, of which RMB3.5 billion was issued by way of a dim sum bond Corporate Governance 2025 KPI Maintain no less than 30% of female representation on our Board 2024 Progress 35.7% of our Board positions are held by female members Disclosures and Recognitions We published our first integrated Climate and Nature-related Financial Disclosures as per Part D: Climate-related Disclosures of the HKEX ESG Code, ISSB IFRS S2 Climate-related Disclosures and TNFD recommendations Ranked No.1 globally, Member of the World Index – 8th consecutive year S&P Sustainability Yearbook Global Sector Leader – 8th consecutive year Ranked No. 1 – 7th consecutive year, “AAA” rating 5 Products that meet specific sustainability criteria such as green certification or accreditation by reputable, independent third parties. 6 Measured by occupied lettable floor area (“LFA”) of office portfolios at 100% basis comprising of Taikoo Place and Pacific Place in Hong Kong and Taikoo Hui Guangzhou. 7 Compared to the 2019 baseline. 8 Compared to the 2018 baseline. 9 Compared to baseline year 2016-2018. Partners Performance (Environment) Performance (Economic) Performance (Environment) Performance (Economic) 10 The 2025 KPIs under Energy have been updated per our approved 1.5°C-aligned SBT. Energy Use Intensity has been renamed to “Electricity Use Intensity” in 2022 to reflect the use of electricity for the provision of shared services for and in the common parts of our buildings. The actual scope of this KPI remains unchanged. 11 Hong Kong portfolio and Chinese Mainland portfolio refer to our office and retail portfolios and hotels in Hong Kong and the Chinese Mainland respectively. 12 Joint venture projects and trading properties are excluded. SEHK:1972 2024-2025 sector leader 2024

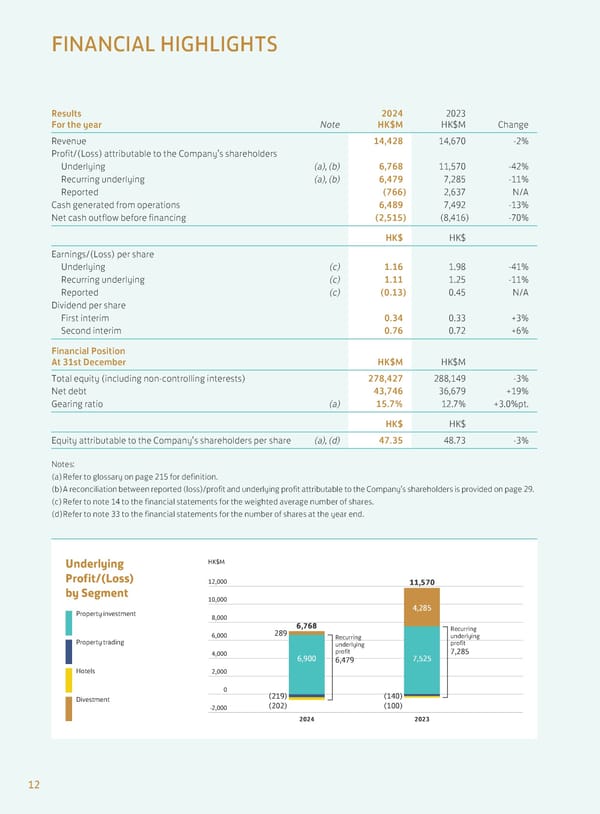

12,000 10,000 8,000 6,000 4,000 2,000 0 -2,000 2024 2023 (219) (202) 6,768 6,900 7,525 289 11,570 4,285 (140) (100) HK$M Property trading Recurring underlying profit 6,479 Recurring underlying profit 7,285 Hotels Property investment Divestment Underlying Profit/(Loss) by Segment 12 Results For the year Note 2024 HK$M 2023 HK$M Change Revenue 14,428 14,670 -2% Profit/(Loss) attributable to the Company’s shareholders Underlying (a), (b) 6,768 11,570 -42% Recurring underlying (a), (b) 6,479 7,285 -11% Reported (766) 2,637 N/A Cash generated from operations 6,489 7,492 -13% Net cash outflow before financing (2,515) (8,416) -70% HK$ HK$ Earnings/(Loss) per share Underlying (c) 1.16 1.98 -41% Recurring underlying (c) 1.11 1.25 -11% Reported (c) (0.13) 0.45 N/A Dividend per share First interim 0.34 0.33 +3% Second interim 0.76 0.72 +6% Financial Position At 31st December HK$M HK$M Total equity (including non-controlling interests) 278,427 288,149 -3% Net debt 43,746 36,679 +19% Gearing ratio (a) 15.7% 12.7% +3.0%pt. HK$ HK$ Equity attributable to the Company’s shareholders per share (a), (d) 47.35 48.73 -3% Notes: (a) Refer to glossary on page 215 for definition. (b) A reconciliation between reported (loss)/profit and underlying profit attributable to the Company’s shareholders is provided on page 29. (c) Refer to note 14 to the financial statements for the weighted average number of shares. (d) Refer to note 33 to the financial statements for the number of shares at the year end. FINANCIAL HIGHLIGHTS

13 SWIRE PROPERTIES ANNUAL REPORT 2024 TEN-YEAR FINANCIAL SUMMARY 2015 HK$M 2016 HK$M 2017 HK$M 2018 HK$M 2019 HK$M 2020 HK$M 2021 HK$M 2022 HK$M 2023 HK$M 2024 HK$M STATEMENT OF PROFIT OR LOSS Revenue Property investment 10,857 10,902 11,380 12,254 12,410 12,635 12,981 12,340 13,525 13,452 Property trading 4,463 4,760 5,833 1,061 516 312 2,443 921 166 88 Hotels 1,127 1,130 1,345 1,404 1,296 641 894 565 979 888 16,447 16,792 18,558 14,719 14,222 13,588 16,318 13,826 14,670 14,428 Profit/(Loss) Attributable to the Company’s Shareholders Property investment 6,231 5,938 6,671 8,732 10,061 8,839 8,654 8,025 7,325 7,234 Property trading 1,089 1,199 1,111 99 (18) (87) 601 171 (169) (233) Hotels (303) (117) (43) (41) (70) (524) (307) (341) (100) (191) Change in fair value of investment properties 7,055 8,030 26,218 19,876 3,450 (4,645) (1,836) 125 (4,419) (7,576) 14,072 15,050 33,957 28,666 13,423 3,583 7,112 7,980 2,637 (766) Dividends for the year 4,154 4,154 4,505 4,914 5,148 5,324 5,558 5,850 6,143 6,379 Retained profit 9,918 10,896 29,452 23,752 8,275 (1,741) 1,554 2,130 (3,506) (7,145) STATEMENT OF FINANCIAL POSITION Net Assets Employed Property investment 235,917 248,466 283,045 299,659 289,185 282,257 288,246 293,752 300,678 289,799 Property trading 7,452 6,616 3,942 4,143 7,789 7,249 9,637 11,612 17,334 26,108 Hotels 7,928 7,520 7,738 7,394 7,229 7,243 6,061 5,841 6,816 6,266 251,297 262,602 294,725 311,196 304,203 296,749 303,944 311,205 324,828 322,173 Financed by Equity attributable to the Company’s shareholders 216,247 225,369 257,381 279,275 286,927 288,216 291,624 289,211 285,082 275,326 Non-controlling interests 1,702 1,856 1,997 2,016 1,984 1,928 1,986 3,047 3,067 3,101 Net debt 33,348 35,377 35,347 29,905 15,292 6,605 10,334 18,947 36,679 43,746 251,297 262,602 294,725 311,196 304,203 296,749 303,944 311,205 324,828 322,173 HK$ HK$ HK$ HK$ HK$ HK$ HK$ HK$ HK$ HK$ Earnings/(Loss) per share 2.41 2.57 5.80 4.90 2.29 0.61 1.22 1.36 0.45 (0.13) Dividends per share 0.71 0.71 0.77 0.84 0.88 0.91 0.95 1.00 1.05 1.10 Equity attributable to shareholders per share 36.97 38.52 44.00 47.74 49.05 49.27 49.85 49.44 48.73 47.35 RATIOS Return on average equity attributable to the Company’s shareholders 6.6% 6.8% 14.1% 10.7% 4.7% 1.2% 2.5% 2.7% 0.9% -0.3% Gearing ratio 15.3% 15.6% 13.6% 10.6% 5.3% 2.3% 3.5% 6.5% 12.7% 15.7% Interest cover – times 13.56 15.48 38.81 33.29 28.85 12.93 20.78 48.26 9.96 1.72 Dividend payout ratio 29.5% 27.6% 13.3% 17.1% 38.4% 148.6% 78.1% 73.3% 233.0% N /A UNDERLYING Profit (HK$M) 7,078 7,112 7,834 10,148 24,130 12,166 9,532 8,706 11,570 6,768 Return on average equity attributable to the Company’s shareholders 3.3% 3.2% 3.2% 3.8% 8.5% 4.2% 3.3% 3.0% 4.0% 2.4% Earnings per share (HK$) 1.21 1.22 1.34 1.73 4.12 2.08 1.63 1.49 1.98 1.16 Interest cover – times 7.75 8.89 10.68 12.58 48.16 32.10 32.96 74.74 26.76 8.92 Dividend payout ratio 58.7% 58.4% 57.5% 48.4% 21.3% 43.8% 58.3% 67.2% 53.1% 94.3% Notes: 1. The information for all years is shown in accordance with the Group’s current accounting policies and disclosure practices. Consequently figures for years prior to 2024 may be different from those originally presented. 2. The equity attributable to the Company’s shareholders and the returns by segment for 2024 and 2023 are shown in the Financial Review – Investment Appraisal and Performance Review on page 80. 3. Underlying profit is discussed on pages 29 to 31. 4. Refer to Glossary on page 215 for definitions and ratios.

350,000 300,000 250,000 200,000 100,000 150,000 50,000 2015 2016 2017 2018 2019 2020 2021 2023 2022 2024 Net Assets Employed HK$M Property investment Property trading Hotels 1.5 2.0 2.5 3.0 3.5 4.0 4.5 1.0 0.0 0.5 2015 2016 2017 2018 2019 2020 2021 2023 2022 2024 Dividends and Underlying Earnings Per Share HK$ Dividends per share Underlying earnings per share 2015 2016 2017 2018 2019 2020 2021 2023 2022 2024 20,000 15,000 10,000 5,000 0 Revenue HK$M Property investment Property trading Hotels 14 TEN-YEAR FINANCIAL SUMMARY

350,000 300,000 250,000 200,000 100,000 150,000 50,000 2015 2016 2017 2018 2019 2020 2021 2023 2022 2024 HK$M Total Equity and Net Debt Total equity Net debt 10 15 5 0 -5 2015 2016 2017 2018 2019 2020 2021 2023 2022 2024 % Returns on Average Equity Group Group – underlying 32,000 40,000 24,000 16,000 8,000 0 -8,000 2015 2016 2017 2018 2019 2020 2021 2023 2022 2024 HK$M Property investment Property trading Hotels Change in fair value of investment properties Total attributable profit/(loss) Total underlying profit Profit/(Loss) Attributable to the Company’s Shareholders 15 SWIRE PROPERTIES ANNUAL REPORT 2024

16 CHAIRMAN’S STATEMENT Despite the ongoing economic uncertainty, we have every confidence that investing in Hong Kong, the Greater Bay Area and the wider Chinese Mainland, as well as South East Asia, continues to be the right thing to do. Dear Shareholders, I am pleased to report that in 2024, Swire Properties gave a positive performance despite adverse market conditions. We remain on track to deliver our long-term investment strategy, and have made significant progress in executing our HK$100 billion strategic investment plan, with 67% already committed. This serves as a clear roadmap for Swire Properties’ growth, setting out our strategic expansion plans across our key markets of Hong Kong, the Chinese Mainland and South East Asia. Our successful capital recycling efforts have provided us with healthy liquidity and place us in a strong position to deliver on the next stages of our investment plan. Last year was also notable for our sustainability achievements. The highlight was achieving the top ranking in the global Dow Jones Best-in-Class World Index 2024 in the ‘Real Estate Management & Development Industry’ category. This recognition reinforces our commitment to advancing our sustainability leadership, innovating and integrating sustainability across all our businesses. Our results reflect the support given by our stakeholders and communities, as well as the team at Swire Properties, and I offer them my thanks. Hong Kong remains our home, and we are committed to playing our part in its ongoing economic recovery. We also anticipate a bright future in the Chinese Mainland, with our investments demonstrating our confidence in the long-term potential in the region. Summary of Financial Results Our recurring underlying profit attributable to shareholders decreased by HK$806 million from HK$7,285 million in 2023 to HK$6,479 million in 2024, which principally reflected higher net finance charges and a reduction in office rental income in Hong Kong. Our underlying profit was HK$6,768 million in 2024, compared to HK$11,570 million in 2023, primarily reflecting the substantial profit arising from the disposal of nine office floors of One Island East in Hong Kong in 2023, and a reduction in profit from the sale of car parking spaces in Hong Kong in 2024. Our reported loss attributable to shareholders in 2024 was HK$766 million, compared to a profit of HK$2,637 million in 2023, mainly due to a fair value loss on investment properties of HK$6,299 million in 2024 compared to HK$4,401 million in 2023. A change in the fair value of investment properties is non-cash in nature and has no impact on our operating cash flows nor on underlying profit attributable to shareholders. Our balance sheet remains healthy. The overall financial position of the Company remains strong and the change in fair value is not expected to have any impact on our investment strategy.

17 SWIRE PROPERTIES ANNUAL REPORT 2024 Place. The completion of the latest phase of the Taikoo Place Redevelopment Project marks a significant milestone for the Company, transforming Taikoo Place into a modern Global Business District and providing a very competitive, credible alternative for tenants traditionally based in Central. Pacific Place continues to attract top-tier tenants despite the challenging operating climate. In the first half of 2025, we will be opening a new bridge connecting Pacific Place to Harcourt Garden, which will significantly improve connectivity to the Admiralty MTR interchange and enhance accessibility in the district. Growth in the Chinese Mainland Recent economic headwinds aside, we remain bullish about our investments and have now secured over 90% of our HK$50 billion planned investment in the Chinese Mainland. The next few years will be dedicated to the completion of our new projects. In Shanghai, our portfolio has expanded to four investments, making it our largest, most important market in the Chinese Mainland to date. In 2024, we unveiled Lujiazui Taikoo Yuan, one of the two mixed-use developments in Shanghai’s Pudong New Area. This project marks the debut of Lujiazui Taikoo Yuan Residences, our first residential project in the Chinese Mainland and which saw a positive response to the initial sales launch. The Shanghai New Bund mixed-use project is also making good progress, having achieved an encouraging sales performance for the four residential towers. Progressive Dividends and Share Buy-Back We declared a second interim dividend for 2024 of HK$0.76 per share. This, together with the first interim dividend of HK$0.34 per share paid in October 2024, amounts to a full year dividend of HK$1.10 per share, representing a 5% increase over the dividend per share for 2023. The second interim dividend for 2024 will be paid on Thursday, 8th May 2025 to shareholders registered at the close of business on the record date, being Thursday, 3rd April 2025. Shares of the Company will be traded ex-dividend from Tuesday, 1st April 2025. Our policy is to deliver sustainable growth in dividends and to pay out approximately half of our underlying profit in ordinary dividends over time. Riding on the benefit of our planned investments, our aim is to deliver mid-single digit annual growth in dividends. Last year, the Board approved a share buy-back programme of up to HK$1.5 billion for the period up to the conclusion of the next annual general meeting to be held in May 2025. During 2024, the Company repurchased 47,778,600 shares for an aggregate cash consideration of HK$750 million at an average price of HK$15.7 per share. Hong Kong Office Portfolio Despite the subdued office market conditions in 2024, the ‘flight-to-quality’ trend remains strong, with prospective tenants favouring new, triple grade-A office buildings like One and Two Taikoo Place and Six Pacific

18 CHAIRMAN’S STATEMENT In Beijing, we are enhancing our Taikoo Li Sanlitun development with the latest renovations catering to the growing demand for luxury retail, as well as supporting the Beijing Government’s initiative to establish the capital as an international consumption centre. The North zone is undergoing extensive upgrading, and The Opposite House hotel site is currently being redeveloped as a new retail landmark for global flagship stores. We are introducing our Taikoo Place brand to Beijing by renaming the Greater INDIGO development as “Taikoo Place Beijing”. Having increased our stake in August 2024, this project now represents our single largest investment in the Chinese Mainland. Taikoo Li Chengdu is undergoing a second wave of trade-mix upgrading, which is now close to completion. Taikoo Li Xi’an will open its sales gallery in 2025, while our retail development in Sanya is also making good progress. We also remain focused on expanding our presence in the Greater Bay Area, given its strategic significance. In Guangzhou, Taikoo Hui Guangzhou, the city’s leading luxury mall, will be expanded by the former Cultural Centre at 387 Tianhe Road, to meet the growing demand from luxury tenants. Taikoo Li Julong Wan Guangzhou, our investment in the retail portion of the transformational mixed-use development, will be launched in phases from the end of 2025. Retail and Residential Overview Our retail malls in Hong Kong have remained resilient despite the challenging market conditions, with all three maintaining full occupancy. Our shopping malls in the Chinese Mainland continue to perform well, with high foot traffic underscoring their appeal as preferred destinations. In Hong Kong, we have spent the past few years building our residential pipeline in the city, and have five projects in various prime locations on Hong Kong Island. In South East Asia, we remain focused on Jakarta, Singapore, Ho Chi Minh City and Bangkok as our core markets. In the Chinese Mainland, we have been delighted by the sales performance of the Shanghai New Bund mixed-use project in Qiantan, and by the positive response to the pre-sales of Lujiazui Taikoo Yuan Residences. Outlook Over the short term, the office market in Hong Kong will likely remain subdued, while retail sales growth in the Chinese Mainland is expected to improve. For the rest of 2025, our priority will be executing our growth plans and enhancing the resilience of our existing portfolios. Despite the ongoing economic uncertainty, we have every confidence that investing in Hong Kong, the Greater Bay Area and the wider Chinese Mainland, as well as South East Asia, continues to be the right thing to do. We remain committed to our key markets and believe we are well- positioned for when conditions improve in the future. Guy Bradley Chairman Hong Kong, 13th March 2025

19 SWIRE PROPERTIES ANNUAL REPORT 2024 CHIEF EXECUTIVE’S STATEMENT Dear Shareholders, As the Chairman has outlined, we have made substantial progress with our HK$100 billion investment plan since 2022. Our focus is now on execution and operational excellence to achieve our growth plans, to enhance profitability and to deliver long-term shareholder returns. Despite significant headwinds in both the office and retail sectors in Hong Kong and the Chinese Mainland, we achieved solid results in 2024. Our business remains resilient and we are well prepared for long-term growth. The latest phase of the Taikoo Place Redevelopment Project is now complete and we have set a new benchmark for the office sector in Hong Kong, alongside our flagship, mixed-use development, Pacific Place. In the Chinese Mainland, the past three years have been marked by high levels of investment activity. Our strong and diverse pipeline of residential, mixed-use and retail-led developments will extend over the next five years, as we continue to increase our gross floor area (“GFA”) in our core markets. In addition, our placemaking strategy has enabled us to support our established projects by acquiring adjacent land or buildings, enabling us to reinforce and enhance each location. Notwithstanding the current weak market conditions, our Company continues to set new standards for the industry and we are well-positioned to face the challenges that lie ahead. We remain committed to accelerating our digital transformation plans and adopting emerging technologies to promote innovation and increase efficiency. 2024 Financial Results at a Glance Our full year result was impacted by the subdued office market in Hong Kong, with a lack of new demand coupled with continuous new supply coming onstream. Our portfolios have continued to demonstrate their resilience, thanks to our strong placemaking attributes, achievements in sustainability, industry-leading amenities and innovative tenant engagement initiatives. Whilst our retail portfolio in Hong Kong experienced a solid recovery in 2023, the performance in 2024 was affected by macro-economic uncertainties. The ongoing trend of outbound travel and changes in tourist spending habits have negatively impacted the retail market. Nevertheless, our shopping malls are in high demand for our major retail tenants, and have achieved full occupancy. We continue to work on enhancing our retail trade mix to adapt to market changes. Our innovative marketing campaigns and loyalty programme initiatives are successfully attracting local shoppers and tourists to our malls. Our HK$100 billion investment plan underscores our commitment to responsible, long-term investments, and we have now been recognised as a global sustainability leader in our field.

20 In 2023, we reached an all-time high in terms of retail sales in the Chinese Mainland, following the easing of pandemic restrictions. Factors such as the weak Japanese yen, increased outbound travel, stock market volatility, and changing consumer behaviours have created an increasingly complex operating environment. Some of our malls have also experienced disruption due to upgrading plans and renovations. Despite these factors and noting the comparison with the high post-pandemic base of the previous year, retail sales growth in the Chinese Mainland has stabilised. At the same time the overall number of visitors to our malls has increased. We recorded an underlying loss from our property trading activities in 2024 due to sales and marketing expenses incurred for several residential trading projects which will be launched over the next few years. Our Future Prospects Office The Hong Kong office market is expected to remain subdued in 2025, with weak demand and oversupply maintaining downward pressure on rents. Despite signs of a modest recovery in Hong Kong’s financial markets, the uncertain economic environment continues to contain new demand for office space. However, the ‘flight-to-quality’ trend remains strong, and our successful placemaking strategy, along with our focus on sustainability, health and safety, and the well-being of tenants’ employees, is highly valued by both existing and prospective tenants. As a result, our office portfolios in Pacific Place and Taikoo Place are well-positioned as the preferred choice for office relocations when the market rebounds. The successful completion of the latest phase of the Taikoo Place Redevelopment Project marks a significant achievement in our Company’s recent history, transforming the district from a former industrial area into a thriving, decentralised office hub and showcasing our commitment to long-term investment in our communities. Our focus on placemaking has been integral to this transformation, providing more open space and landscaped areas, including Taikoo Square, Taikoo Garden, and Taikoo Park, all interconnected with the ten office buildings. The activation of these spaces through ground-floor retail, restaurants, and year-round community events has created a sense of wellbeing and vibrancy for tenants and visitors, redefining work-life balance. Our integrated planning approach and ongoing efforts in placemaking and placekeeping are key advantages, and have been fundamental in realising our vision for Taikoo Place as a Global Business District. Looking ahead, we remain committed to upgrading and offering new products to maintain our competitive advantage. While the market is currently oversupplied, we are reviewing the timing for redevelopment of the Wah Ha Factory Building and Zung Fu Industrial Building to reflect market conditions. CHIEF EXECUTIVE’S STATEMENT

21 SWIRE PROPERTIES ANNUAL REPORT 2024 Retail Footfall and retail sales in Hong Kong are expected to continue to face challenges due to outbound travel and changing tourist spending habits. However, we are optimistic about the resilience of our shopping malls, thanks to the continued refinement of our trade mix, robust marketing campaigns and innovative loyalty programmes. Our malls have benefitted from clear market positioning, attracting both local and international customers. We are committed to maintaining a vibrant and diverse trade mix and elevating the retail experience to capture the full market potential. The Christmas campaign at Pacific Place attracted record-breaking numbers of visitors, particularly from the Chinese Mainland. We are confident that the Government’s multi-entry visa policy will benefit the market. Footfall in our Chinese Mainland malls has continued to increase, highlighting their appeal as desirable retail landmarks. Retail sales stabilised in Q4 2024, reflecting improved consumer sentiment following the Government’s stimulus measures which were announced in September 2024. In 2025, retail sales growth is expected to pick up in the Chinese Mainland, driven by increased domestic demand and the progressive completion of renovation work in several malls. Inbound and outbound travel activity is expected to increase, together with a shift in spending behaviour compared to pre-pandemic patterns. In the long-term, onshore consumption is expected to dominate the retail market in the Chinese Mainland, with the number of luxury customers continuing to grow, thereby establishing the Chinese Mainland as one of the largest luxury markets globally. Demand for retail space in 2025 is expected to remain selective. Luxury retailers will adopt a prudent approach to expanding in Beijing, Chengdu, and Shanghai, seeking high- potential, experiential locations. In Guangzhou, demand for suitable locations for luxury brands is expected to be sustained while overall demand for sports and leisure brands is increasing. Structural and reconfiguration works are ongoing at Taikoo Li Sanlitun North in Beijing and at HKRI Taikoo Hui in Shanghai as a key part of our asset reinforcement strategy. We are also making good progress with our pipeline of new, mixed-use projects in Sanya, Xi’an, two projects in Shanghai and our two newest projects, the former Cultural Centre adjacent to Taikoo Hui Guangzhou and Taikoo Li Julong Wan Guangzhou, our latest retail project located in Liwan district. We are also introducing our flagship Taikoo Place brand to Beijing, repositioning Greater INDIGO as “Taikoo Place Beijing”, to be rolled out in phases from mid-2026. Residential In Hong Kong, residential sales have increased due to interest rate cuts and relaxed mortgage measures. However, rebuilding confidence and restoring market sentiment will take time. Medium to long-term demand is expected to improve, supported by local buyers and increasing interest from Chinese Mainland buyers. We have a balanced trading pipeline in Hong Kong, and pre-sale plans are underway for our latest project, The Headland Residences, in Chai Wan.

22 CHIEF EXECUTIVE’S STATEMENT The residential market for high-quality developments in prime locations in Tier-1 cities in the Chinese Mainland is expected to remain strong in the short term, as evidenced by the successful sales of Lujiazui Taikoo Yuan Residences in Shanghai in Q4 2024. The long-term outlook for Shanghai’s luxury residential market is positive. Thanks to several key factors including urbanisation, a growing middle class and the limited supply of luxury properties, residential markets are expected to improve in Jakarta, Ho Chi Minh City, and Bangkok. In Miami the luxury residential market remains robust, with South Florida attracting homebuyers due to its favourable climate, tax regime and strategic location as the gateway to Latin America. Hotels The speed of recovery for our hotels in Hong Kong has been slower than expected. In contrast, our hotels in the Chinese Mainland remained relatively stable while our managed hotel in Miami performed well. The outlook for our hotel business in Hong Kong is cautiously optimistic, depending on the rate of recovery of international tourists and business travellers. In the Chinese Mainland, our hotel business is expected to improve steadily in 2025. In accordance with our strategy to expand the hotel business through Hotel Management Agreements, we have several new hotels coming onstream over the next few years, including in Beijing, Shenzhen, Shanghai, Xi’an and Tokyo. Sustainability Leadership We have demonstrated global leadership in sustainable development, earning the highest ranking in the Dow Jones Best-in-Class World Index 2024. Our efforts have been further recognised with top positions in other indices and benchmarks, including the Global Real Estate Sustainability Benchmark (“GRESB”) and the Hang Seng Corporate Sustainability Index. We have been named Global Sector Leader – Listed (Mixed Use) in GRESB for the eighth consecutive year and ranked No.1 in the Hang Seng Corporate Sustainability Index for the seventh year in a row, maintaining the highest “AAA” rating. Our journey towards net-zero emissions is on track, driven by digital innovation and the adoption of new technologies. In 2024, we increased our off-site renewable electricity procurement for our Beijing portfolio to nearly 100%. Consequently, over 60% of electricity consumption in our Chinese Mainland portfolio now comes from renewable energy. We continue to engage our tenants and suppliers through impactful initiatives like the Green Performance Pledge (“GPP”) programme and Green Kitchen Initiative (“GKI”). In 2024 we launched the Green Retail Partnership (“GRP”) Framework to focus on sustainable shop design and performance improvements. In November, we entered into a partnership with LVMH under the GRP to elevate sustainability performance across their stores, offices and F&B locations in the Chinese Mainland and Hong Kong.

23 SWIRE PROPERTIES ANNUAL REPORT 2024 The opening of Taikoo Square in 2024 marked a major milestone in realising our vision for urban biodiversity, showcasing our ambitious work in biophilic design and nature-based placemaking at Taikoo Place in Hong Kong. In 2024, our community investment initiatives made a significant contribution. Through our Community Ambassador Programme, over 3,000 ambassadors dedicated their time to various community projects. In particular, our signature “Books for Love” campaign raised over HK$1.3 million for charity, whilst promoting literacy and reducing waste in the city. We also held the “LITTLE FASHION FOR LOVE” event at the Quarryside community centre, in partnership with St. James’ Settlement’s Green Little, raising awareness amongst the younger generation about sustainable fashion. We continue to empower youth through diverse programmes that foster creativity, leadership, and community engagement, preparing them to shape a sustainable future. In 2024, the Swire Properties Placemaking Academy organised our largest ever White Christmas Street Fair in numerous locations around Taikoo Place, attracting more than 80,000 visitors over five days and supporting local businesses and district tourism. Additionally, the Bi-city Youth Cultural Leadership Programme, now in its third edition, engaged 130 university students from Beijing and Hong Kong, fostering cultural exchange and nurturing future leaders. Outlook Despite the challenging market conditions, we are making good progress on many fronts. Our HK$100 billion investment plan underscores our commitment to responsible, long-term investments, and we have now been recognised as a global sustainability leader in our field. We greatly appreciate the continued support of our shareholders and all our partners. I would also like to express my sincere gratitude to the team at Swire Properties for their collective efforts which have contributed so significantly to our achievements this year. Tim Blackburn Chief Executive Hong Kong, 13th March 2025

24 1. Create long-term value by conceiving, designing, developing, owning and managing transformational mixed-use and other projects in urban areas With our long-term placemaking vision, we will continue to design projects which we believe will have the necessary scale, mix of uses and transport links to become key commercial destinations and to transform the areas in which they are situated. 2. Maximise the earnings and value of our completed properties through active asset management and by reinforcing our assets through enhancement, redevelopment and new additions We manage our completed properties actively (including by optimising the mix of retail tenants and early renewal negotiations with office tenants) and with a view to the long term, to maintain consistently high levels of service and to enhance and reinforce our assets. By doing so, we believe that we will maximise the occupancy and earnings potential of our properties. Tenants increasingly scrutinise the sustainable development credentials of landlords and buildings. We aim to be at the forefront of sustainable development by incorporating relevant design As a leading developer, owner and operator of mixed-use, principally commercial, properties in Hong Kong and the Chinese Mainland, our strategic objective is sustainable growth in shareholder value in the long term. To achieve this objective, we employ five strategies. KEY BUSINESS STRATEGIES

25 SWIRE PROPERTIES ANNUAL REPORT 2024 elements, technologies and programmes to improve our performance in Environment, Social and Governance, and by engagement with tenants and others with whom we do business. 3. Develop luxury and high-quality residential property activities Our residential developments will be aimed at buyers of luxury and high-quality properties, where we believe we have a competitive advantage. We will look to acquire appropriate sites for trading and investment with reasonable returns in the markets in Hong Kong. We will seek residential development opportunities in the Chinese Mainland. These are likely to be ancillary to our mixed-use developments. However, in the right locations and cities we may also consider standalone residential development opportunities. We will also actively explore residential trading opportunities in four target markets of Jakarta, Singapore, Bangkok and Ho Chi Minh City in South East Asia. 4. Focus principally on Hong Kong and the Chinese Mainland In Hong Kong, we will continue to focus on reinforcing our existing investment property assets and on seeking new sites suitable for transformative developments and for residential projects. In Chinese Mainland, we will expand our presence with large-scale mixed-use, commercial developments in Tier-1 and emerging Tier-1 cities. We will continue to leverage our established “Taikoo Li” and “Taikoo Hui” brands to develop iconic landmark properties. While we will continue to concentrate on Hong Kong and the Chinese Mainland, we intend to expand selectively in South East Asia. 5. Manage our capital base conservatively We intend to maintain a strong balance sheet supported by an active capital recycling strategy, with a view to investing in and financing our projects in a disciplined and targeted manner. We aim to maintain exposure to a range of debt maturities and a range of debt types and lenders. Our current debt profile reflects a mix of revolving and term bank loans and medium term notes. In implementing the above strategies, the principal risks and uncertainties facing by the Group are that the economies in which it operates (in particular Hong Kong and the Chinese Mainland) will not perform as well in the future as they have in the past and the uncertainties as to whether this will happen.

Lujiazui Taikoo Yuan Residences Show Flat, Shanghai MANAGEMENT DISCUSSION & ANALYSIS

28 2024 HK$M 2023 HK$M Revenue Gross Rental Income derived from Office 5,488 5,835 Retail 7,388 7,143 Residential 440 430 Other Revenue (1) 136 117 Property Investment 13,452 13,525 Property Trading 88 166 Hotels 888 979 Total Revenue 14,428 14,670 Operating Profit/(Losses) derived from Property investment From operations 8,250 8,261 Sale of interests in investment properties (220) (60) Fair value losses in respect of investment properties (5,996) (2,829) Property trading (178) (89) Hotels (154) (103) Total Operating Profit 1,702 5,180 Share of Post-tax Profit/(Losses) from Joint Venture and Associated Companies 826 (292) (Loss)/Profit Attributable to the Company’s Shareholders (766) 2,637 (1) Other revenue is mainly estate management fees. Additional information is provided in the following section to reconcile reported and underlying profit attributable to the Company’s shareholders. These reconciling items principally adjust for the fair value movements on investment properties and the associated deferred tax in the Chinese Mainland and the U.S.A., and for other deferred tax provisions in relation to investment properties. In Hong Kong, the Group’s investment properties recorded fair value losses of HK$9,207 million in 2024. In the Chinese Mainland and the U.S.A., investment properties recorded fair value gains of HK$2,647 million and HK$341 million respectively. There are further adjustments to remove the effect of the movement in the fair value of the liability in respect of a put option in favour of the owner of a non-controlling interest, remeasurement gains on interests in joint venture companies which became subsidiary companies after completion of acquisition and a bargain purchase gain arising from the acquisition of an additional interest in a joint venture company. Amortisation of right-of-use assets classified as investment properties is charged to underlying profit. REVIEW OF OPERATIONS

29 SWIRE PROPERTIES ANNUAL REPORT 2024 Underlying Profit Reconciliation Note 2024 HK$M 2023 HK$M (Loss)/Profit Attributable to the Company’s Shareholders per Financial Statements (766) 2,637 Adjustments in respect of investment properties: Fair value losses in respect of investment properties (a) 6,219 4,392 Deferred tax on investment properties (b) 1,283 461 Fair value gains realised on sale of interests in investment properties (c) 534 4,398 Depreciation of investment properties occupied by the Group (d) 22 22 Non-controlling interests’ share of fair value movements less deferred tax 76 8 Movement in the fair value of the liability in respect of a put option in favour of the owner of a non-controlling interest (e) 55 39 Remeasurement gains on interests in joint venture companies which became subsidiary companies after completion of acquisition (f) – (306) Reversal of impairment loss on a hotel held as part of a mixed-use development (g) (11) – Bargain purchase gain arising from the acquisition of an additional interest in a joint venture company (h) (566) – Less amortisation of right-of-use assets reported under investment properties (i) (78) (81) Underlying Profit Attributable to the Company’s Shareholders 6,768 11,570 Profit from divestment (289) (4,285) Recurring Underlying Profit Attributable to the Company’s Shareholders 6,479 7,285 Notes: (a) This represents the fair value movements as shown in the Group’s consolidated statement of profit or loss and the Group’s share of fair value movements of joint venture and associated companies. (b) This represents deferred tax movements on the Group’s investment properties, plus the Group’s share of deferred tax movements on investment properties held by joint venture and associated companies. These comprise deferred tax on fair value movements on investment properties in the Chinese Mainland and the U.S.A., and deferred tax provisions made in respect of investment properties held for the long-term where it is considered that the liability will not reverse for some considerable time. It also includes certain tax adjustments arising from transfers of investment properties within the Group. (c) Prior to the implementation of HKAS 40, changes in the fair value of investment properties were recorded in the revaluation reserve rather than the consolidated statement of profit or loss. On sale, fair value gains/(losses) were transferred from the revaluation reserve to the consolidated statement of profit or loss. (d) Prior to the implementation of HKAS 40, no depreciation was charged on investment properties occupied by the Group. (e) The value of the put option in favour of the owner of a non-controlling interest is calculated principally by reference to the estimated fair value of the portion of the underlying investment property in which the owner of the non-controlling interest is interested. (f) The remeasurement gains on interests in joint venture companies were calculated principally by reference to the estimated market value of the underlying properties portfolio of the joint venture companies, netting off with all related cumulative exchange difference. (g) Under HKAS 40, hotel properties are stated in the accounts at cost less accumulated depreciation and any provision for impairment losses, rather than at fair value. If HKAS 40 did not apply, wholly-owned and joint venture hotel properties held for the long-term as part of mixed-use property developments would be accounted for as investment properties. Accordingly, any increase or decrease in their values would be recorded in the revaluation reserve rather than in the consolidated statement of profit or loss. (h) Bargain purchase gain arising from the acquisition of an additional interest in a joint venture company was calculated principally by reference to the market value of the underlying properties portfolio of the joint venture company in comparison with the consideration paid. (i) HKFRS 16 amends the definition of investment property under HKAS 40 to include properties held by lessees as right-of-use assets to earn rentals or for capital appreciation or both, and requires the Group to account for such right-of-use assets at their fair value. The amortisation of such right-of-use assets is charged to underlying profit.

2023 2024 12,000 2,000 4,000 6,000 8,000 10,000 0 -3,996 -625 -79 -102 6,768 11,570 HK$M Movement in Underlying Profit Underlying profit in 2023 Decrease in profit from divestment Decrease in profit from property investment Increase in loss from property trading Increase in loss from hotels Underlying profit in 2024 30 MANAGEMENT DISCUSSION & ANALYSIS REVIEW OF OPERATIONS Underlying Profit Our reported loss attributable to shareholders in 2024 was HK$766 million, compared to a profit of HK$2,637 million in 2023. There was a fair value loss on investment properties (after deducting non-controlling interests) of HK$6,299 million in 2024, compared to HK$4,401 million in 2023, mainly arising from the Hong Kong office portfolios for both years. Underlying profit attributable to shareholders (which principally adjusts for changes in fair value of investment properties) decreased by HK$4,802 million from HK$11,570 million in 2023 to HK$6,768 million in 2024. The decrease primarily reflected the substantial profit arising from the disposal of certain office floors in Hong Kong in 2023, and a reduction in profit from the sale of car parking spaces in Hong Kong in 2024. Also, there were higher net finance charges (due to higher borrowings) and a reduction in rental income from Hong Kong office portfolios. Recurring underlying profit (which excludes profit from divestment) was HK$6,479 million in 2024, compared to HK$7,285 million in 2023. Recurring underlying profit from property investment decreased in 2024. This principally reflected lower office rental income from Hong Kong (partly due to the loss of revenue arising from the disposal of nine floors of One Island East in December 2023). In Hong Kong, office market remained difficult. Weak demand, high vacancy rates and new supplies continued to exert downward pressure on office rent. Despite these challenges, the occupancy of the office portfolio remained steady and outperformed the relevant submarkets. The performance of retail portfolio was soft. Trade mix improvement, marketing campaigns and loyalty programme initiatives were continuously and actively carried out to attract local customers and tourists, so as to offset the negative impact of outbound travel and the changing tourist spending behaviour. In the Chinese Mainland, the performance of our retail portfolio was stable. Retail sales declined in 2024 (compared with a strong rebound in 2023 following the lifting of pandemic-related restrictions) but the overall foot traffic increased notwithstanding the increase in outbound travel. In the U.S.A., retail sales and gross rental income increased compared to 2023, primarily due to an improved tenant mix and higher opening rate. The underlying loss from property trading in 2024 was primarily a result of sales and marketing expenses incurred for several residential trading projects which will be launched in the next few years. The speed of recovery of hotel businesses in Hong Kong was slower than anticipated, while the performance of the hotels in the Chinese Mainland was relatively stable. Performance of the managed hotel in the U.S.A. was strong.

300,000 200,000 250,000 150,000 100,000 50,000 0 2015 2016 2017 2018 2019 2020 2021 2023 2022 2024 HK$M Valuation of Investment Properties Completed Under development 14,000 12,000 10,000 8,000 4,000 6,000 2,000 0 2015 2016 2017 2018 2019 2020 2021 2023 2022 2024 HK$M Gross Rental Income (After Deduction of Rental Concessions) Hong Kong office Hong Kong retail Hong Kong residential Chinese Mainland U.S.A. and elsewhere 27,000 21,000 24,000 18,000 15,000 9,000 6,000 3,000 12,000 0 -3,000 2015 2016 2017 2018 2019 2020 2021 2023 2022 2024 HK$M Underlying Operating Profit Property investment Property trading Hotels Divestment 31 SWIRE PROPERTIES ANNUAL REPORT 2024

2031 2032 2024 2025 2026 2027 2028 2030 2029 40,000 35,000 30,000 25,000 15,000 20,000 5,000 10,000 0 GFA (000 sq. ft.) Attributable Completed Investment Property and Hotel Portfolio by Location Hong Kong Chinese Mainland U.S.A. Beyond 2032 40,000 35,000 30,000 25,000 15,000 20,000 10,000 5,000 0 2031 2032 2024 2025 2026 2027 2028 2030 2029 GFA (000 sq. ft.) Attributable Completed Investment Property and Hotel Portfolio by Type Office Retail Hotels/Residential/ Serviced apartments Under planning Beyond 2032 50 40 30 20 10 0 Target (HK$ Bn) HK$100 Billion Investment Plan Hong Kong Commitment for new projects 67% COMMITTED Committed Remaining target Chinese Mainland Residential trading projects (including in South East Asia) 32 MANAGEMENT DISCUSSION & ANALYSIS REVIEW OF OPERATIONS

33 SWIRE PROPERTIES ANNUAL REPORT 2024 In March 2022, the Company announced a plan to invest HK$100 billion over ten years in development projects in Hong Kong and the Chinese Mainland, and in residential trading projects (including in South East Asia). The target allocation is HK$30 billion to Hong Kong, HK$50 billion to the Chinese Mainland and HK$20 billion to residential trading projects (including in South East Asia). At 7th March 2025, approximately HK$67 billion of the planned investments had been committed (HK$11 billion to Hong Kong, HK$46 billion to the Chinese Mainland and HK$10 billion to residential trading projects). Major committed projects include the residential developments at The Headland Residences (formerly known as Chai Wan Inland Lot No. 178), at 269 Queen’s Road East, at 983-987A King’s Road and 16-94 Pan Hoi Street in Hong Kong, and at Wireless Road in Bangkok, a retail-led mixed-use development in Xi’an, a retail-led development in Sanya, mixed-use developments in Lujiazui Taikoo Yuan (formerly known as the Yangjing Mixed-use Project) and the New Bund in Shanghai, the retail portion of a mixed-use development in Guangzhou (Taikoo Li Julong Wan Guangzhou), the extension of Taikoo Hui to No. 387 Tianhe Road in Guangzhou, office and other commercial use developments at 8 Shipyard Lane and at 1067 King’s Road in Hong Kong. Uncommitted projects include further retail-led mixed-use projects in Tier-1 and emerging Tier-1 cities in the Chinese Mainland, including Beijing, with a plan to double our gross floor area in the Chinese Mainland, further expansion at Pacific Place and Taikoo Place in Hong Kong as well as further residential trading projects in Hong Kong, the Chinese Mainland, Miami and South East Asia. Key Developments In February 2024, the Group obtained the occupation permit for Six Pacific Place, it being the newest addition to Pacific Place, an office tower with an aggregate GFA of approximately 223,000 square feet. At 31st December 2024, the office tower was 53% let. Handover of the office floors to tenants is in progress. As part of a mixed-use development with an approximate GFA of 5.7 million square feet located in Liwan district of Guangzhou, the centre of the Guangzhou-Foshan metropolis circle, the Group is collaborating with the Guangzhou Pearl River Enterprises Group to develop the retail portion (“Taikoo Li Julong Wan Guangzhou”) of this mixed-use development. The site with a GFA of approximately 352,000 square feet was acquired as of 31st December 2024. The GFA will increase to approximately 1,615,000 square feet, subject to further relevant transaction agreements. Basement works are in progress. The overall development is planned to be completed in phases beginning from the first half of 2027. Prior to the first phase’s completion, exhibitions, events, pop-up shops and activities will be conducted to activate the area starting from late 2025. The Group has a 50% interest in the retail portion of the development. In June 2024, the Group entered into an equity and debt transfer agreement with the China Life Insurance Company Limited (“China Life”) group and the Sino-Ocean Group Holding Limited (“Sino-Ocean”) group, pursuant to which the Group and the China Life group have conditionally agreed to acquire a 14.895% and a 49.895% equity interest in the project company of Taikoo Place Beijing (formerly known as INDIGO Phase Two), respectively, from the Sino-Ocean group for a consideration of approximately RMB891 million and RMB2,984 million, respectively. The acquisitions were completed in early August. Following completion of the acquisitions, the Group’s interest in Taikoo Place Beijing has increased from 35% to 49.895% and the China Life group owns a 49.895% interest in Taikoo Place Beijing. Taikoo Place Beijing has been renamed from INDIGO Phase Two since November 2024.

34 MANAGEMENT DISCUSSION & ANALYSIS REVIEW OF OPERATIONS Completed Investment Properties and Hotels (GFA attributable to the Group in million square feet) Office Retail Hotels(1) Residential/ Serviced Apartments Under Planning Total Hong Kong 9.4 2.6 0.8 0.6 – 13.4 Chinese Mainland 2.9 6.2 1.1 0.2 – 10.4 U.S.A. – 0.3 0.3 – – 0.6 Total 12.3 9.1 2.2 0.8 – 24.4 In August 2024, Taikoo Hui in Guangzhou successfully bid for No. 387 Tianhe Road in a public auction, which is connected to its shopping mall. With approximate GFA of 655,000 square feet, No. 387 Tianhe Road will be refurbished as a luxury retail addition to Taikoo Hui, which is expected to complete from 2027. The Group has a 97% interest in this property. In December 2024, an associated company in which the Group holds a 40% interest started the pre-sales of the first batch of Lujiazui Taikoo Yuan Residences, a residential development in Shanghai, with 49 out of 50 units pre-sold up to 7th March 2025. Portfolio Overview The aggregate gross floor area (“GFA”) attributable to the Group at 31st December 2024 was approximately 40.4 million square feet. Of the aggregate GFA attributable to the Group, approximately 35.2 million square feet are investment properties and hotels, comprising completed investment properties and hotels of approximately 24.4 million square feet, and investment properties under development or held for future development of approximately 10.8 million square feet. In Hong Kong, the investment property and hotel portfolio comprise approximately 14.2 million square feet attributable to the Group of primarily Grade-A office and retail premises, hotels, serviced apartments and other luxury residential accommodation. In the Chinese Mainland, the Group has interests in eleven major commercial developments in prime locations in Beijing, Guangzhou, Chengdu, Shanghai, Xi’an and Sanya. These developments are expected to comprise approximately 18.9 million square feet of attributable GFA when they are all completed. Of this, 10.4 million square feet has already been completed. Outside of Hong Kong and the Chinese Mainland, the investment property portfolio comprises the Brickell City Centre development in Miami, U.S.A. The tables below illustrate the GFA (or expected GFA) attributable to the Group of the investment property and hotel portfolio at 31st December 2024.

35 SWIRE PROPERTIES ANNUAL REPORT 2024 Investment Properties and Hotels Under Development or Held for Future Development (expected GFA attributable to the Group in million square feet) Office Retail Hotels(1) Residential/ Serviced Apartments Under Planning Total Hong Kong – – – – 0.8 0.8 Chinese Mainland 2.2 3.5 0.2 0.1 2.5 8.5 U.S.A. – – – – 1.5(2) 1.5 Total 2.2 3.5 0.2 0.1 4.8 10.8 Total Investment Properties and Hotels (GFA (or expected GFA) attributable to the Group in million square feet) Office Retail Hotels(1) Residential/ Serviced Apartments Under Planning Total Total 14.5 12.6 2.4 0.9 4.8 35.2 (1) Hotels are accounted for in the financial statements under property, plant and equipment and, where applicable, the leasehold land portion is accounted for under right-of-use assets. (2) This property is accounted for under properties held for development in the financial statements. The trading portfolio comprises completed units available for sale at EIGHT STAR STREET and LA MONTAGNE in Hong Kong. There are nine residential projects under development, four in Hong Kong, two in the Chinese Mainland, one in Indonesia, one in Vietnam and one in Thailand. There is also a plan to develop a luxury residential and hospitality project on part of our land banks in Miami, U.S.A. The table below illustrates the GFA (or expected GFA) attributable to the Group of the trading property portfolio at 31st December 2024. Trading Properties (GFA (or expected GFA) attributable to the Group in million square feet) Completed Development(1) Under Development or Held for Development Total Hong Kong 0.1 1.0 1.1 Chinese Mainland – 1.0 1.0 U.S.A. and elsewhere – 3.1 3.1 Total 0.1 5.1 5.2 (1) Completed development in Hong Kong comprises EIGHT STAR STREET and LA MONTAGNE.

56% 42% 2% 54% 43% 3% Hong Kong Chinese Mainland U.S.A. Completed Investment Properties GFA (Excl. Hotels) 31st December 2023 31st December 2024 58% 40% 2% 56% 41% 3% Hong Kong Chinese Mainland U.S.A. Attributable Gross Rental Income Year ended 31st December 2023 Year ended 31st December 2024 74% 23% 3% 73% 24% 3% Hong Kong Chinese Mainland U.S.A. and elsewhere Net Assets Employed 31st December 2023 31st December 2024 36 MANAGEMENT DISCUSSION & ANALYSIS REVIEW OF OPERATIONS The charts below show the analysis of the Group’s completed investment properties GFA (excluding hotels), gross rental income and net assets employed by region on an attributable basis.

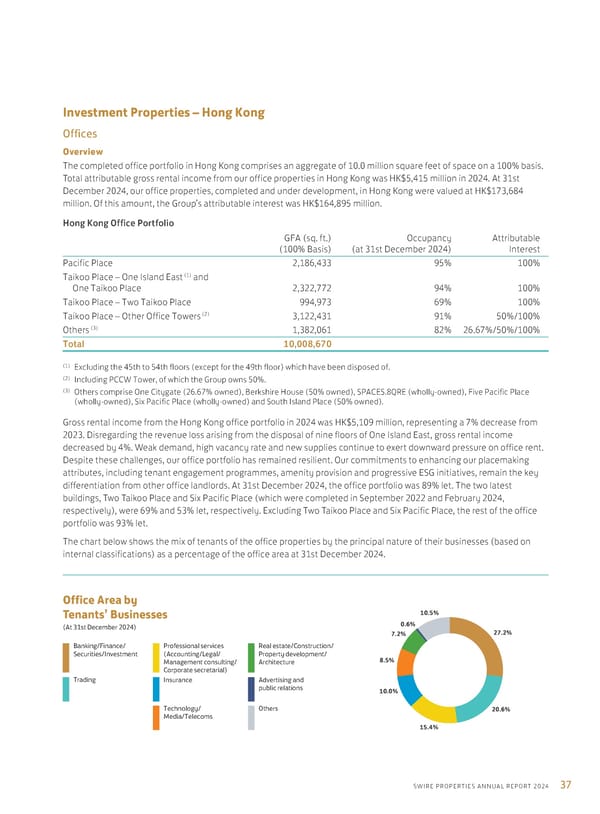

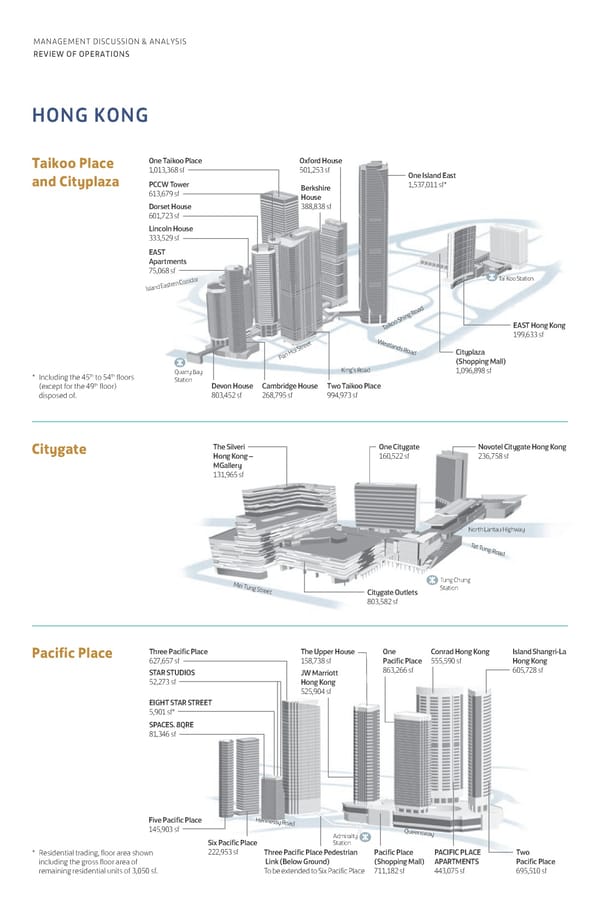

27.2% 15.4% 8.5% 7.2% 20.6% 10.0% 0.6% 10.5% Banking/Finance/ Securities/Investment Trading Professional services (Accounting/Legal/ Management consulting/ Corporate secretarial) Insurance Technology/ Media/Telecoms Real estate/Construction/ Property development/ Architecture Advertising and public relations Others Office Area by Tenants’ Businesses (At 31st December 2024) 37 SWIRE PROPERTIES ANNUAL REPORT 2024 Investment Properties – Hong Kong Offices Overview The completed office portfolio in Hong Kong comprises an aggregate of 10.0 million square feet of space on a 100% basis. Total attributable gross rental income from our office properties in Hong Kong was HK$5,415 million in 2024. At 31st December 2024, our office properties, completed and under development, in Hong Kong were valued at HK$173,684 million. Of this amount, the Group’s attributable interest was HK$164,895 million. Hong Kong Office Portfolio GFA (sq. ft.) (100% Basis) Occupancy (at 31st December 2024) Attributable Interest Pacific Place 2,186,433 95% 100% Taikoo Place – One Island East (1) and One Taikoo Place 2,322,772 94% 100% Taikoo Place – Two Taikoo Place 994,973 69% 100% Taikoo Place – Other Office Towers (2) 3,122,431 91% 50%/100% Others (3) 1,382,061 82% 26.67%/50%/100% Total 10,008,670 (1) Excluding the 45th to 54th floors (except for the 49th floor) which have been disposed of. (2) Including PCCW Tower, of which the Group owns 50%. (3) Others comprise One Citygate (26.67% owned), Berkshire House (50% owned), SPACES.8QRE (wholly-owned), Five Pacific Place (wholly-owned), Six Pacific Place (wholly-owned) and South Island Place (50% owned). Gross rental income from the Hong Kong office portfolio in 2024 was HK$5,109 million, representing a 7% decrease from 2023. Disregarding the revenue loss arising from the disposal of nine floors of One Island East, gross rental income decreased by 4%. Weak demand, high vacancy rate and new supplies continue to exert downward pressure on office rent. Despite these challenges, our office portfolio has remained resilient. Our commitments to enhancing our placemaking attributes, including tenant engagement programmes, amenity provision and progressive ESG initiatives, remain the key differentiation from other office landlords. At 31st December 2024, the office portfolio was 89% let. The two latest buildings, Two Taikoo Place and Six Pacific Place (which were completed in September 2022 and February 2024, respectively), were 69% and 53% let, respectively. Excluding Two Taikoo Place and Six Pacific Place, the rest of the office portfolio was 93% let. The chart below shows the mix of tenants of the office properties by the principal nature of their businesses (based on internal classifications) as a percentage of the office area at 31st December 2024.

38 MANAGEMENT DISCUSSION & ANALYSIS REVIEW OF OPERATIONS At 31st December 2024, the top ten office tenants (based on attributable gross rental income in the twelve months ended 31st December 2024) together occupied approximately 23% of the Group’s total attributable office area in Hong Kong. Pacific Place The offices at One, Two, and Three Pacific Place showed resilience in 2024. These offices were 95% let at 31st December 2024. New tenants included Hongkong Tianyi, VC Asset Management, Hemin Asset Management, Wellington Legal, Progeny, Arquitectonica, Three Capital Partners, Shikhara Capital, Cook Asia Limited, Emirates Shipping, and Carret Private Capital. Existing tenants including FWD Life Insurance, Moelis, Charles Russell, Willsun Fertility Hong Kong, and Richard Mille expanded their spaces. Renewals were notable among tenants such as Bank of Japan, Innova Strategies, Orient Wealth, China Huarong Overseas, CPE Advisors, Sculptor Capital, Moody’s, Schroders, Neo Derm, Interactive Brokers, Woori Bank, Visa, Alpine Investment Management, Wells Fargo Bank, Tencent, Goodman, Old Peak, KVB Trading, and Richard Mille. John Swire & Sons, Centurium Capital, Cabral Investment, Mackenzie Investments, Eight Roads, and Northern Trust confirmed relocations within the portfolio upon lease expiry. KGI committed to a consolidation of its group companies in the portfolio alongside decade-long lease renewals from the anchor tenants of Deloitte and PAG. At Six Pacific Place, the occupation permit was obtained in February 2024, and the building was 53% let at 31st December 2024, with commitments from Sotheby’s, Bonhams, British American Tobacco, PineBridge Investments, Dun & Bradstreet, Arrowpoint Investment Partners, and Hugill & Ip. Taikoo Place The performance of One Taikoo Place and One Island East (excluding the nine floors disposed of) at Taikoo Place was steady. These two offices towers were 97% and 92% let, respectively, at 31st December 2024. In One Taikoo Place, AXA Investment Managers and MetLife Asia renewed their leases. In One Island East, CHANEL and Squarepoint Capital leased more space. Accenture, AllianceBernstein, Aon Hong Kong Limited, Capgemini, Covestro, Cushman & Wakefield, H&H Group and Swift renewed their leases. TAIKOO PLACE H O N G KO N G

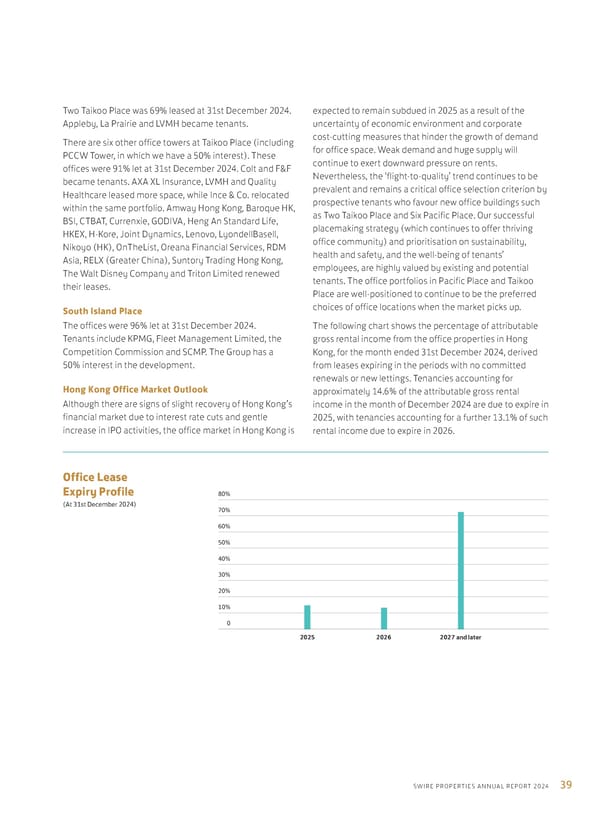

2025 2026 70% 80% 60% 50% 40% 30% 10% 20% 0 Office Lease Expiry Profile (At 31st December 2024) 2027 and later 39 SWIRE PROPERTIES ANNUAL REPORT 2024 Two Taikoo Place was 69% leased at 31st December 2024. Appleby, La Prairie and LVMH became tenants. There are six other office towers at Taikoo Place (including PCCW Tower, in which we have a 50% interest). These offices were 91% let at 31st December 2024. Colt and F&F became tenants. AXA XL Insurance, LVMH and Quality Healthcare leased more space, while Ince & Co. relocated within the same portfolio. Amway Hong Kong, Baroque HK, BSI, CTBAT, Currenxie, GODIVA, Heng An Standard Life, HKEX, H-Kore, Joint Dynamics, Lenovo, LyondellBasell, Nikoyo (HK), OnTheList, Oreana Financial Services, RDM Asia, RELX (Greater China), Suntory Trading Hong Kong, The Walt Disney Company and Triton Limited renewed their leases. South Island Place The offices were 96% let at 31st December 2024. Tenants include KPMG, Fleet Management Limited, the Competition Commission and SCMP. The Group has a 50% interest in the development. Hong Kong Office Market Outlook Although there are signs of slight recovery of Hong Kong’s financial market due to interest rate cuts and gentle increase in IPO activities, the office market in Hong Kong is expected to remain subdued in 2025 as a result of the uncertainty of economic environment and corporate cost-cutting measures that hinder the growth of demand for office space. Weak demand and huge supply will continue to exert downward pressure on rents. Nevertheless, the ‘flight-to-quality’ trend continues to be prevalent and remains a critical office selection criterion by prospective tenants who favour new office buildings such as Two Taikoo Place and Six Pacific Place. Our successful placemaking strategy (which continues to offer thriving office community) and prioritisation on sustainability, health and safety, and the well-being of tenants’ employees, are highly valued by existing and potential tenants. The office portfolios in Pacific Place and Taikoo Place are well-positioned to continue to be the preferred choices of office locations when the market picks up. The following chart shows the percentage of attributable gross rental income from the office properties in Hong Kong, for the month ended 31st December 2024, derived from leases expiring in the periods with no committed renewals or new lettings. Tenancies accounting for approximately 14.6% of the attributable gross rental income in the month of December 2024 are due to expire in 2025, with tenancies accounting for a further 13.1% of such rental income due to expire in 2026.

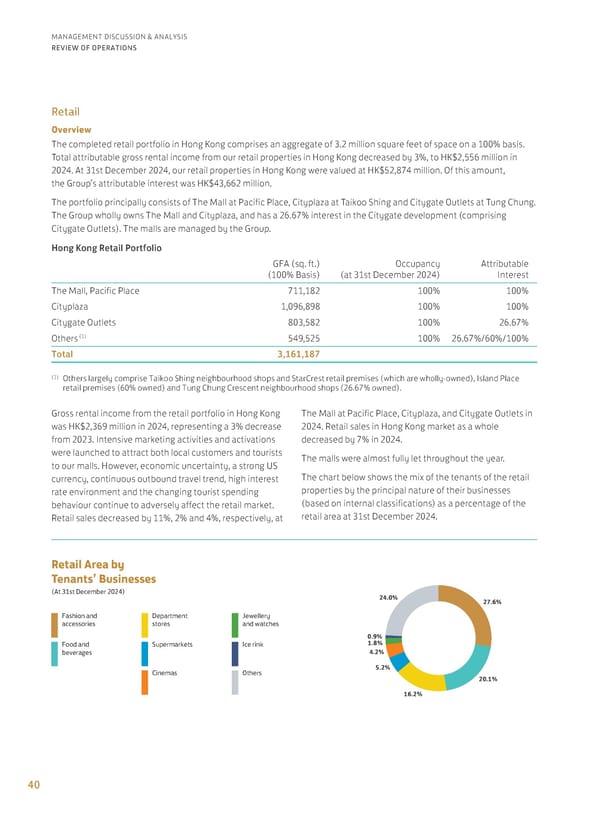

27.6% 16.2% 4.2% 1.8% 20.1% 24.0% 5.2% 0.9% Fashion and accessories Food and beverages Department stores Supermarkets Cinemas Jewellery and watches Ice rink Others Retail Area by Tenants’ Businesses (At 31st December 2024) 40 MANAGEMENT DISCUSSION & ANALYSIS REVIEW OF OPERATIONS Retail Overview The completed retail portfolio in Hong Kong comprises an aggregate of 3.2 million square feet of space on a 100% basis. Total attributable gross rental income from our retail properties in Hong Kong decreased by 3%, to HK$2,556 million in 2024. At 31st December 2024, our retail properties in Hong Kong were valued at HK$52,874 million. Of this amount, the Group’s attributable interest was HK$43,662 million. The portfolio principally consists of The Mall at Pacific Place, Cityplaza at Taikoo Shing and Citygate Outlets at Tung Chung. The Group wholly owns The Mall and Cityplaza, and has a 26.67% interest in the Citygate development (comprising Citygate Outlets). The malls are managed by the Group. Hong Kong Retail Portfolio GFA (sq. ft.) (100% Basis) Occupancy (at 31st December 2024) Attributable Interest The Mall, Pacific Place 711,182 100% 100% Cityplaza 1,096,898 100% 100% Citygate Outlets 803,582 100% 26.67% Others (1) 549,525 100% 26.67%/60%/100% Total 3,161,187 (1) Others largely comprise Taikoo Shing neighbourhood shops and StarCrest retail premises (which are wholly-owned), Island Place retail premises (60% owned) and Tung Chung Crescent neighbourhood shops (26.67% owned). Gross rental income from the retail portfolio in Hong Kong was HK$2,369 million in 2024, representing a 3% decrease from 2023. Intensive marketing activities and activations were launched to attract both local customers and tourists to our malls. However, economic uncertainty, a strong US currency, continuous outbound travel trend, high interest rate environment and the changing tourist spending behaviour continue to adversely affect the retail market. Retail sales decreased by 11%, 2% and 4%, respectively, at The Mall at Pacific Place, Cityplaza, and Citygate Outlets in 2024. Retail sales in Hong Kong market as a whole decreased by 7% in 2024. The malls were almost fully let throughout the year. The chart below shows the mix of the tenants of the retail properties by the principal nature of their businesses (based on internal classifications) as a percentage of the retail area at 31st December 2024.

41 SWIRE PROPERTIES ANNUAL REPORT 2024 On, and Polo Ralph Lauren & Ralph’s Coffee became tenants. CHANEL, COS, Goyard, Jaeger-LeCoultre, lululemon, MUJI and Watsons have expanded, while André Fu Living, Kelly & Walsh, Moynat, O.N.S, Puyi Optical and Tumi have relocated. The premises occupied by Aigle, American Vintage, BEYØRG®|ORGANIC SPA and Repetto were refitted. Cityplaza Cityplaza is the largest shopping mall on Hong Kong Island, with a total floor area of approximately 1.1 million square feet. The six-level mall has more than 170 shops and restaurants, a cinema, an indoor ice rink and over 800 indoor parking spaces. Continued improvements to the tenant mix, promotions and activities in the mall make it a one-stop lifestyle hub for shopping, dining and entertainment. At 31st December 2024, the top ten retail tenants (based on attributable gross rental income in the twelve months ended 31st December 2024) together occupied approximately 26% of the Group’s total attributable retail area in Hong Kong. The Mall at Pacific Place The Mall at Pacific Place is in the mixed-use Pacific Place development. The offices and the four hotels at Pacific Place provide a flow of shoppers for The Mall. The Mall was fully let. Despite a more competitive retail environment, tenant mix refinement and store upgrade to improve customer experience remain the key strategies. New retail and F&B brands were introduced. Anteprima Wirebag, Arc’teryx, Billionaire Boys Clubs/ICECREAM, Chicha San Chen, Descente, Jacadi, Little Cove Expresso, Maison Margiela, Manolo Blahnik, Messika, Open Dialogue, PACIFIC PLACE H O N G KO N G